2023 global equity returns were dominated by an alphabet soup of megatrends. From (Chat)GPT shining the spotlight on the lifechanging potential of Generative Artificial Intelligence (GEN AI), to a broader adoption of Glucagon-Like Peptide -1 (GLP-1) diabetes drugs for weight loss and other obesity-related diseases. These megatrends resulted in extraordinary share price movements across multiple sectors as investors crowded into the themes and quickly decided who the winners and losers may be.

As we head into the third month of 2024, we continue to see these megatrends dominate equity market returns. In contrast to 2023, there is a clear bifurcation between megatrend beneficiaries that can deliver revenue and earnings growth and those that can’t. This is not only evident within the Magnificent 7 (“Mag 7”), but also across other so-called GEN AI and GLP-1 winners and losers.

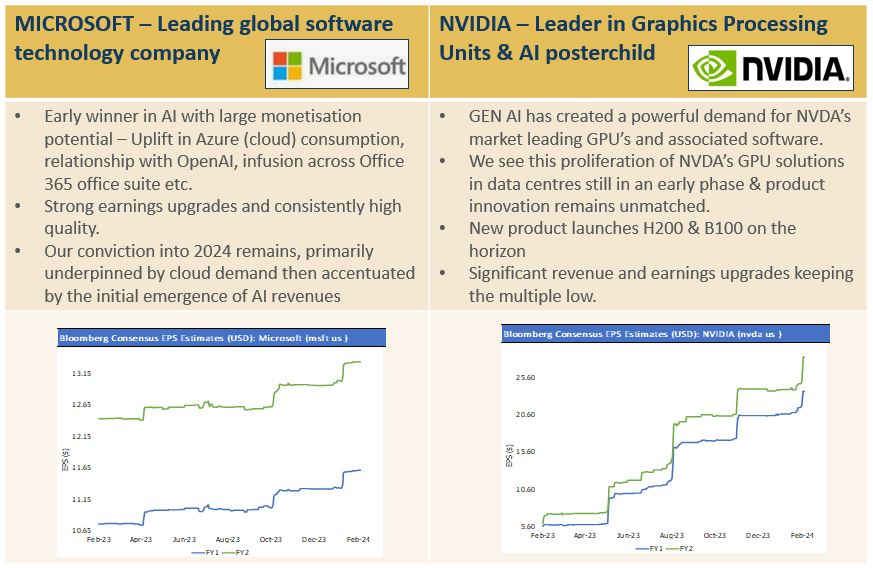

Alphinity continues to have selective exposure across both megatrends. Within GEN AI, we have exposure to early AI winners, such as Nvidia and Microsoft. In addition, we continue to invest in opportunities across the broader AI ecosystem. SK Hynix, ASML, Cadence and Accenture are examples of technology enablers and facilitators where AI is augmenting company performance. Importantly, we continue to look further afield across sectors to companies not only enabling AI but those that will also reap its benefits.

We also have a nuanced exposure to the GLP-1 megatrend where the initial market clamour to define “winners” and “losers” delivered some interesting opportunities. While market leader and key GLP-1 winner, Novo Nordisk, has seen strong share price gains, assisted robotic surgery company Intuitive Surgical was initially dropped into the loser bucket on account of minor exposure to gastric banding. The market has since recalibrated ISRG expectations, and the shares have more than recovered the initial knee jerk reaction.

A further broadening out of these megatrends should continue to create exciting new “show me” opportunities in 2024 and beyond.

GEN AI – Show me the earnings

GEN AI truly entered our lives in 2023. OpenAI’s humanlike generative AI Chatbot, ChatGPT kicked off a wave of excitement across consumers and companies. What ensued was a whirlwind of AI investments and developments across multiple industries as companies explored different ways of delivering AI building blocks or integrating these technologies into their businesses.

During 2023, many companies in the AI ecosystem got swept up in the euphoria. From the enablers and infrastructure providers on the front end (such as semiconductor makers and data centres) to those that design software and provide related services (including end-user applications and cloud computing), amongst others. None more so than the Mag 7.

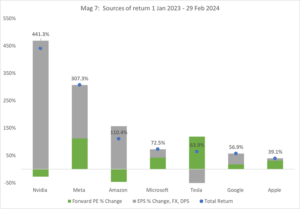

While 2023 saw the rising AI tide lift most Mag 7 boats, year-to-date there has been a large divergence in performance amongst the group, defined by those that can deliver earnings growth to justify high multiples and those who can’t. AI posterchild, Nvidia, has added another c60% YTD, to be up more than 440% since the start of 2023. Importantly, during this time the Nvidia forward PE multiple has come down, from 44x to 32x. The stock has got cheaper as earnings have outstripped the remarkable share price growth. Other major enablers such as Amazon and Microsoft have continued to rally supported by strong results from increased AI demand also.

Meanwhile Tesla and Apple have been dethroned by GLP-1 winner Eli Lilly and AI winner ASML, who now occupy their top 7 spots in YTD contributors. Both Tesla and Apple are facing a range of challenges, but also recently disappointed investors with the lack of progress with their AI related plans.

Bifurcation within the Mag 7 driven by strong earnings power or the lack thereof: Nvidia derated despite 441% return over the 14 months

Source: Bloomberg, 29 February 2024

While industry data suggest a rapid adoption of AI across industries, the enablers continue to lead the charge year-to-date. Recent 4Q23 result releases and capex intentions underscore the longevity of investment intentions across enablers and adopters. AI mentions were at all-time highs as AI diffusion becomes more commonplace and remains a top CIO priority.

While AI is emerging as one of the largest innovation cycles in decades, we are only in the early innings of its diffusion. It will take time for AI to impact revenues and margins more meaningfully and more broadly.

Microsoft company quote 4Q23 results: “We are also the leader in low-code/no-code development, helping everyone create apps, automate workflows, analyze data and now build custom copilots. More than 230,000 organizations have already used AI capabilities in Power Platform, up over 80% quarter over quarter.”

Alphinity’s exposure to GEN AI – A selective approach

Throughout 2023 and into 2024, Alphinity has maintained a selective exposure to the AI ecosystem. We own 4 of the Mag 7 early AI winners (Nvidia, Microsoft, Alphabet and Amazon) for their exposure to various AI segments, including semiconductors, cloud, datacentres, large language models and other applications. Complimented with other AI technology building blocks, including design (Cadence), equipment suppliers (ASML), memory chip manufacturers (SK Hynix) and other services (Accenture).

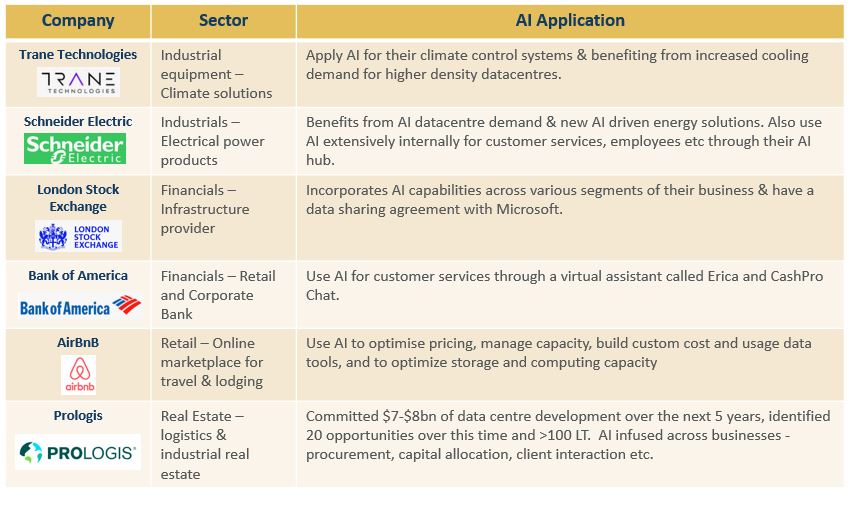

Importantly, we continue to look further afield. To companies producing the building blocks of the building blocks. And others using AI effectively to expand their product offering and improve productivity and efficiencies. Interesting examples include Trane Technologies, Prologis, AirBnb, and London Stock Exchange.

These stocks have all recently delivered strong 4Q23 results and continue to enjoy earnings upgrades.

Alphinity has a balanced exposure to Gen AI through selective beneficiaries: Within the Mag 7…

Source: Alphinity, Bloomberg, 29 February 2024

Within Tech beyond the Mag 7

Source: Alphinity, Bloomberg, 29 February 2024

…..and further afield in AI infused opportunities

Source: Alphinity, 29 February 2024

GLP-1 Therapies – Show me the results

2023 was also a breakthrough year for Glucagon Like Peptide-1 (GLP-1) or diabesity therapies. Two landmark clinical trials showed that GLP-1 drugs, already discovered in 1987, not only let people lose weight, but also produced meaningful health benefits beyond weight loss itself.

Believers flocked to buy the two market leaders, US based Eli Lilly (the manufacturer of Mounjaro) and Danish listed Novo Nordisk (the manufacturer of Ozempic, Wegovy). In contrast they shunned businesses that grew with the global population waistline fuelled by comments from corporates, such as Walmart, on initial signs of consumer behaviour changes. This resulted in hundreds of billions of dollars of market cap difference between these “GLP1 winners” and the so-called “GLP1 losers”.

Walmart CEO John Furner: “we have seen a slight pullback in overall baskets from people taking GLP-1 and other appetite suppressing medications”

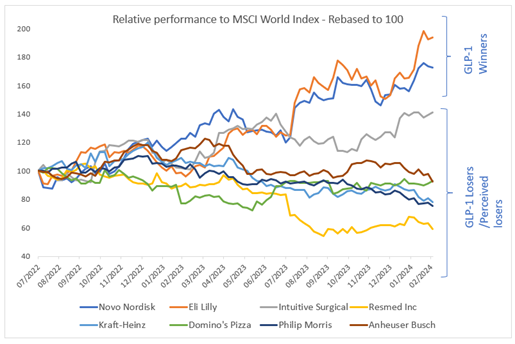

The hardest hit sector was the medical device sector as these companies serve patients who suffer from chronic conditions related to obesity. Examples include global robotics surgery leader, Intuitive Surgical and global sleep apnoea equipment maker ResMed. Equally fast-food chains, such as Domino’s pizza, processed food producers such as Kraft, and Beer and Tobacco companies like Anheuser Busch and Phillip Morris, also came under pressure as surveys and studies showed GLP-1 patients shifting to healthier foods and habits.

Year-to-date we have continued to see diverging trends between GLP-1 winners and “losers”

Source: Bloomberg, 29 February 2024

Alphinity’s exposure to GLP-1 – A balanced approach

Against the backdrop of an increasing global obesity problem and a modest adoption of GLP-1 drugs to date (c6.5m users vs more than 1 billion people with obesity globally), we anticipate an acceleration in the use of GLP-1’s. Long-term ramifications could be far reaching across various industries, but changes won’t happen overnight. Treatments are currently expensive (cUS$1000 per month in the USA), supply is limited, and health insurance companies are not providing wide ranging coverage.

While many of the perceived ‘GLP-1 losers’ have recovered from the initial knee-jerk selling pressure, we still expect an ongoing impact from GLP-1 headlines in 2024 and beyond, particularly around intake innovation (development of a pill format) and updates on health insurance coverage of those drugs.

Despite the outperformance over the last year, we continue to see upside in GLP-1 winner, Novo Nordisk. With big investments in additional capacity, new trial outcomes scheduled from April 2024 onwards and continued innovation, we expect Novo to continue to defend their current 80-90% combined market share (with Eli Lilly) for years to come in this ultra-growth market. This class of drugs is in a very interesting part of its cycle, with medical trials starting to show their potential positive impact on other medical conditions (cardio, kidney, sleep apnea etc). The total long-term market potential for GLP-1 drugs is still expanding.

On the other hand, despite being initially defined as a GLP-1 loser, Intuitive Surgical continues to demonstrate the value of its robotic assisted surgery technology and provides a complimentary MedTech exposure to the portfolio. The GLP-1 narrative is also shifting in MedTech, to one where increased longevity from GLP-1 use may be a tailwind rather than the pure headwind initially defined.

Alphinity is invested in GLP-1 winners (Novo Nordisk) and innovative Med tech (Intuitive Surgical)

Source: Alphinity, Bloomberg, 29 February 2024

Conclusion

In times when the stock market is infused with captivating megatrends, such as GEN AI and GLP-1, there is a tendency for investor expectations to overshoot. Resulting in share prices of perceived beneficiaries running on speculation and the fear-of-missing-out rather than fundamentals. The intense market concentration and diverging price movements of the last 14 months is a good case in point.

Looking ahead, we expect to see a continuous evolvement and adoption of both GEN AI and GLP-1. Assessing long term winners and losers along the way will be crucial and fluid. At Alphinity, we will continue to deploy our agile, tested investment process to find “show me” megatrend earnings leaders in 2024 and beyond.

Author: Elfreda Jonker, Client Portfolio Manager