Last month, BHP made it onto the front page for the wrong reasons.

A Four Corners story, followed by Guardian coverage, raised questions about whether BHP was quietly walking back its emissions commitments.

For us, that was a moment to pause and ask: does this change our view?

So we refreshed our work

BHP is an over-weight holding across our strategies. As active owners, we engage with the company regularly on transition risk and other material ESG topics – in this half alone we have spoken to the company seven times on ESG matters. But rather than rely on existing analysis, or simply react to the headlines, we went back to first principles.

Using BHP’s ESG Databook, Integrated Annual Report and Climate Transition Action Plan, we built a bottom-up, asset-level view of its emissions profile, recent trends and realistic pathways to FY30. The work tested where emissions are concentrated, how BHP is tracking against its target, the ambition of that target, what different transition scenarios imply, and how its approach to diesel compares with peers.

What enabled us to do this analysis

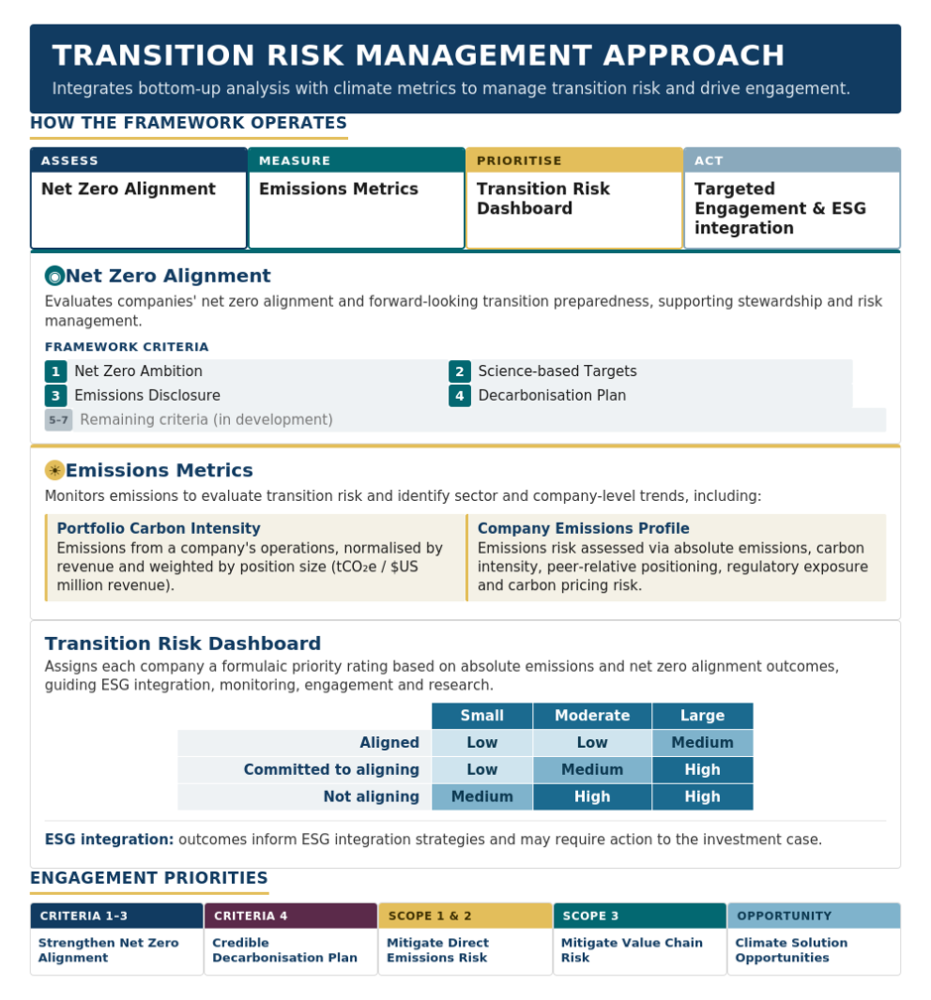

Transition risk has been core to how we assess investments for years. When we became signatories to the Net Zero Asset Managers Initiative, we enhanced our transition risk management approach and developed a Net Zero Alignment Framework that was integrated into our overall approach to managing climate risk. This framework evaluates net zero ambition, science-based targets, emissions disclosure and decarbonisation plan quality. BHP has been assessed under this framework since 2024.

Layered on top was the bespoke scenario analysis tool we built in 2025, integrating over 50 scenarios and mapping them against company emissions targets and performance. This ongoing work meant we already had a base to build from when the headlines hit — and the analytical infrastructure to go deeper quickly when it mattered.

The following graphic illustrates our transition risk management approach.

What we found

Using our asset level analysis along with insights from our discussion with the company we have a clearer, asset-level view of where BHP’s emissions sit today and a credible line of sight to its FY30 target.

1. BHP is broadly on track for FY30. The headline number is encouraging: operational emissions are down 36% since FY20, ahead of BHP’s 30% FY30 target on a point-in-time basis. But the cumulative carbon budget gives a more balanced view. BHP has used just over half of its FY20–FY30 budget, and our scenario work suggests it can still meet both the FY30 endpoint and cumulative budget under a range of transition conditions. We see that as broadly on track, rather than clearly ahead.

2. The progress so far has been real, but uneven across assets. Much of the early emissions reduction has come from renewable power agreements in Chile, particularly at Escondida and Pampa Norte. Outside those assets, performance is more mixed: some operations are broadly flat, Western Australia Iron Ore has edged higher, BMA (BHP Mitsubishi Alliance) has benefited from asset changes and improved methane measurement, and Western Australia Nickel fell sharply after its FY25 suspension. This matters because the group result can look stronger than the underlying asset-by-asset picture.

3. Diesel is the real transition challenge. Diesel now dominates BHP’s operational emissions profile, making up 68% of group Scope 1 and 2 emissions and around 80% of Scope 1 emissions in FY25. That makes it the central post-2030 decarbonisation question. BHP has consistently positioned diesel abatement as a later-decade challenge, but investors now need more clarity on trials, timing, capital requirements, productivity impacts and the role of governments and equipment manufacturers in making alternatives viable at scale.

4. Asset-level analysis matters. A group target is useful, but it can hide very different transition risks across the portfolio. Diesel, electricity and methane each need different solutions, and the viability of alternatives varies by region, altitude, ore type, haulage profile, connectivity, charging infrastructure, OEM delivery timelines and safety requirements. BHP’s detailed asset-level reporting gave us the data to look beyond the headline target and assess where the real risks sit, including the trade-off between moving quickly and paying the cost of being first.

5. Emissions intensity is still part of the picture. BHP’s target is set on an absolute emissions basis, which is important because the atmosphere responds to tonnes, not ratios. But emissions intensity still matters for investors. It helps show how efficiently BHP is producing relative to peers, how changes in production volumes may affect the trajectory, and whether improvements are coming from genuine operational efficiency or portfolio shifts. BHP should be encouraged to integrate this perspective into its next Climate Transition Action Plan and set of targets

What this means for our view on BHP

The recent headlines prompted the review, but it didn’t decide the outcome.

Once we built our own asset-level emissions model, the picture that emerged was more nuanced: genuine progress in one region, a flat retained asset base elsewhere, and a diesel transition that continues to be challenging.

Our analysis of transition risk looks at both net zero alignment and emissions footprints, because either lens on its own only tells half the story. We want the companies we own to transition — but we also want them to do it in a financially disciplined way, rather than rushing into commitments or capital decisions that don’t hold up.

On that basis, BHP remains as a medium priority under our Transition Risk Management Approach: ‘committed to aligning’ to net zero, with a moderate emissions footprint relative to the rest of our portfolio (illustrated below).

That’s where our view sits today: comfortable with BHP’s trajectory on the data, but watching closely for how the diesel transition actually plays out — for BHP and for the sector more broadly.

Where to from here

The next phase of our work is to extend this analysis beyond FY30 and model BHP’s emissions pathway through to 2050. We want to use scenario analysis to better test the company’s forward climate transition plan, including the pace of diesel abatement, the role of technology, the timing of asset-level reductions and the assumptions behind its long-term emissions forecast. This will help us move from asking whether BHP can meet its interim target, to whether its broader pathway is credible, investable and aligned with the transition risks we see across the portfolio.

For more information on our approach to responsible investing see our 2025 Responsible Investment Report.