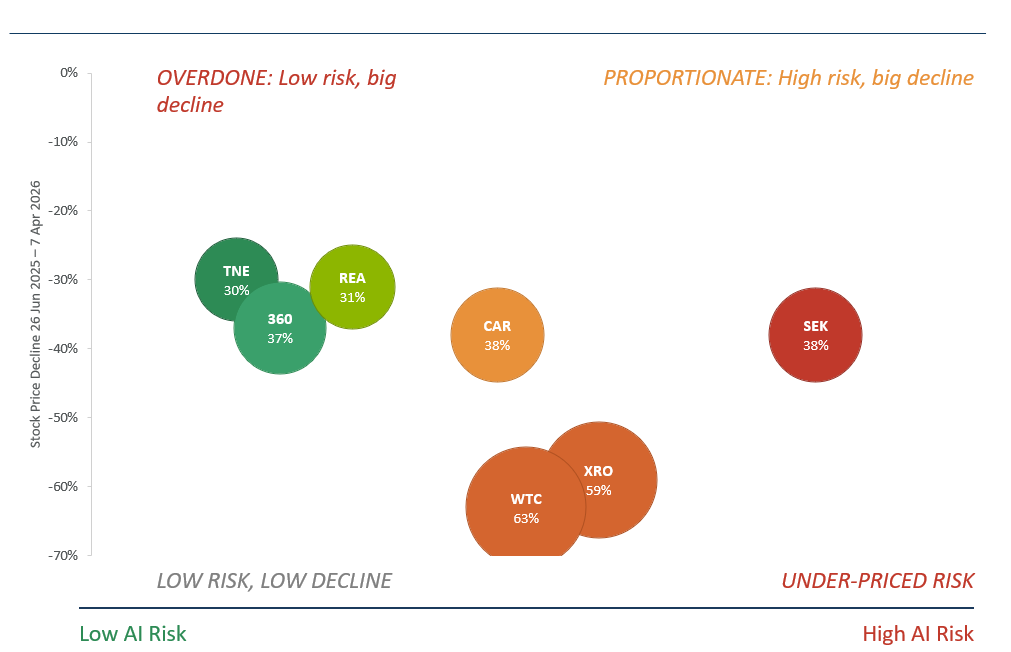

AI is the most significant structural force reshaping technology investing. But disruption is not binary. The same structural force that threatens some business models is creating opportunities for others. The market’s broad derating of some ASX sectors, in particular software technology and digital platforms, has created a meaningful disconnect between price and risk — and we think that disconnect cuts in both directions.

At Alphinity, we have developed a systematic framework to assess AI disruption risk to long term earnings power of companies across our investable universe. Below, we share the framework, the results, and four case studies that illustrate both extremes — the protected and the threatened.

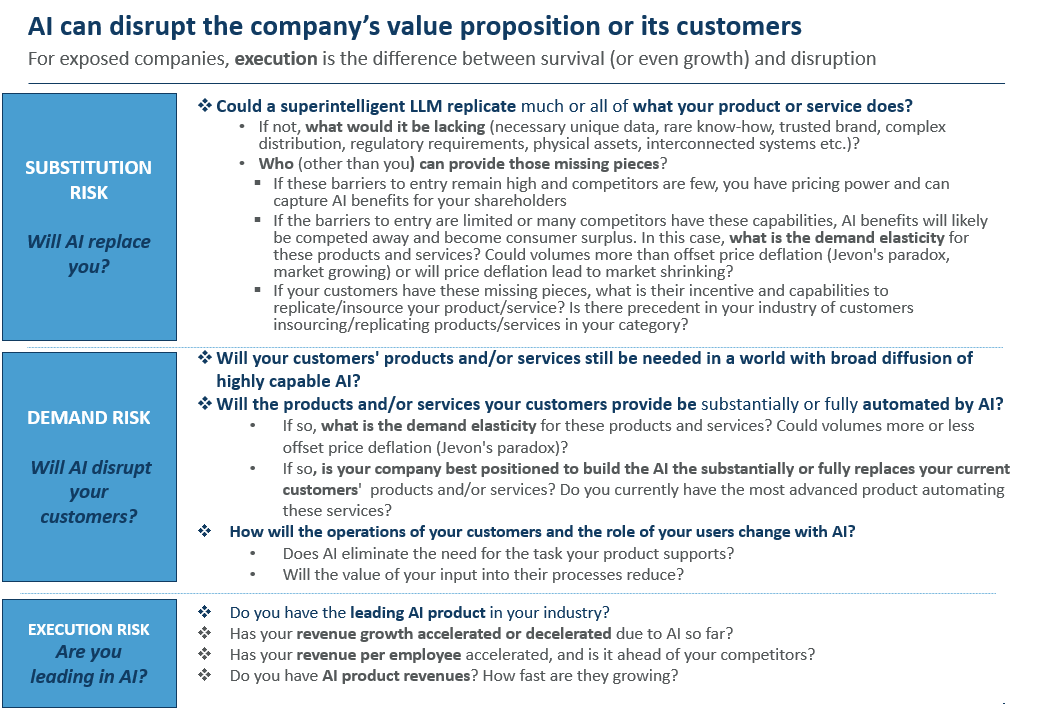

We assess every business through three risk lenses: AI disruption exposure framework

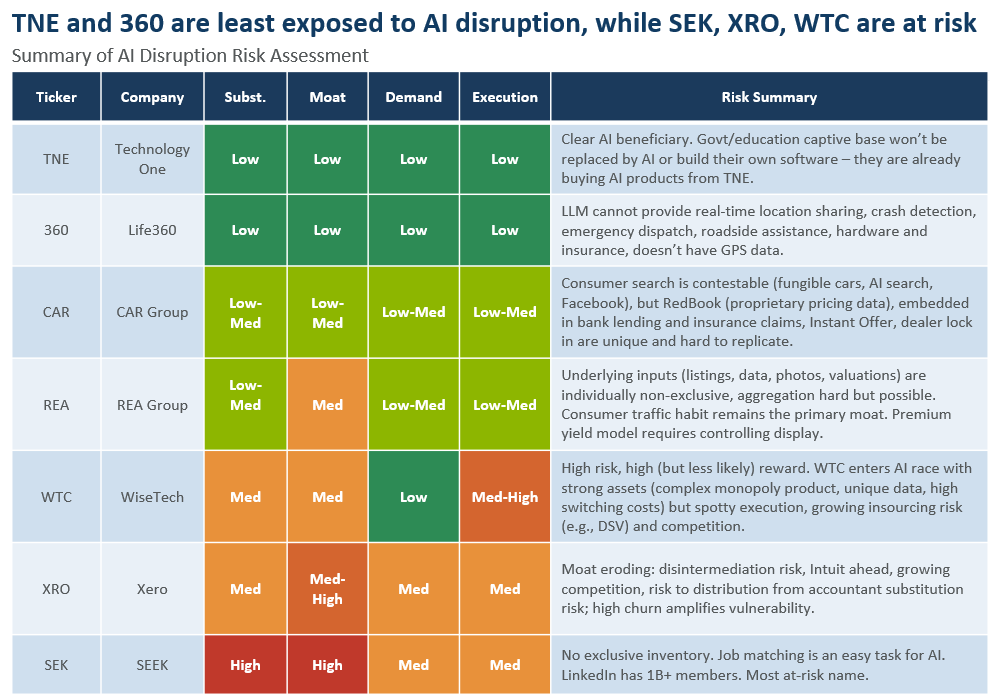

Applying the framework across seven ASX-listed technology companies yields a clear spectrum. The market has initially treated these businesses as a monolith, with only some differentiation starting to emerge of late; we think the differences matter.

The results: ASX tech from least to most exposed

AI Disruption Risk Assessment – a clear spectrum of outcomes

Case studies: the spectrum in practice

The matrix sets out our view across the coverage universe. The case studies below explain the reasoning behind two names that sit at opposite ends of the spectrum — TechnologyOne, which ranked as the least exposed, and SEEK, which ranked as the most.

Least impacted : TechnologyOne (TNE) OWNED — The Moat That AI Strengthens

Applying our AI disruption framework to TechnologyOne, what stood out was not just the resilience of the business model — but the extent to which AI is becoming a tangible growth driver

Why AI cannot substitute it:

TNE is an integrated ERP platform — financials, HR/payroll, student management, asset management, and regulatory reporting — sold into government, education, and healthcare across Australia, New Zealand, the UK, and Asia. Over 73% of ANZ residents live in a council powered by TNE software.

The product is a system of record: an auditable compliance backbone with 35+ years of sector-specific regulatory configuration baked into its code. Government procurement panels, sovereign data residency requirements, and multi-year implementation cycles create switching costs that no competitor — AI-native or otherwise — can shortcut. An LLM can generate a financial report, but it cannot be the certified general ledger behind it, nor can it navigate the procurement frameworks, data residency rules, and compliance obligations that make TNE the only credible choice for its customer base. In addition to this product and regulatory complexity, TNE customers are highly risk averse (in Australia local government leaders are personally liable for their decisions in their official capacity) and not profit driven, which makes the prospect of switching to an alternative provider, even if one emerged, that much less likely.

Why AI is accelerating the earnings cycle:

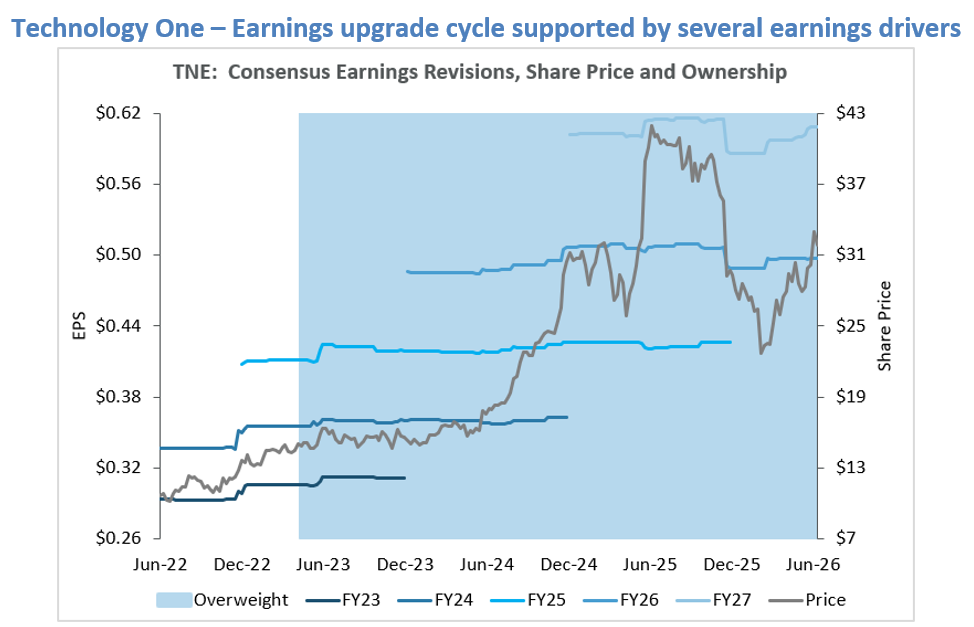

Where most enterprise software companies are defending against AI, TNE is selling it. The Plus product applies agentic AI across the enterprise suite on a usage-based pricing model — creating a transactional ARR layer on top of the SaaS base that did not exist twelve months ago. Eight deals were signed before the product officially launched in March 2026. In February 2026, TNE reaffirmed upgraded FY26 guidance — PBT growth 18–20%, ARR growth 16–18%., with all FY26 AI investment included in existing R&D and a 2ppt margin improvement targeted for FY26 as benefits of AI help to drive profitability. Longer term, the company is targeting $1bn + ARR & AI Revenue by FY30.

The Guide product extends AI further — to end-consumers, residents, and students — expanding TNE’s surface area from back-office infrastructure into community engagement.

The investment case: multiple compounding growth vectors

The AI resilience story is reinforced by a business with multiple independent growth drivers. SaaS Plus is reshaping the revenue model — charging a permanent ARR uplift rather than a one-time implementation fee — building a higher-quality, more recurring revenue base over time. The UK local government opportunity is large: councils there fulfil a broader range of functions than their Australian counterparts, the incumbent landscape is fragmented legacy software with no integrated alternative, and a wave of council consolidation is creating natural displacement events that TNE is well-placed to capture. Continued wins in student management, Australian federal government, and new products including DXP and the app platform provide additional growth levers extending earnings upgrade cycle.

What to watch:

The key metrics are Plus deal signings and conversion rates as the product moves from pre-launch pipeline to live implementations, UK council win rates during the consolidation cycle, and how quickly and materially transactional revenue from Plus begins ramping up. Quality and momentum are both strong. The earnings upgrade cycle has multiple remaining chapters.

Outcome:

AI stress-testing not only validated the investment case but identified an additional earnings driver the market is still under-pricing. TNE is the clearest example in our analysis of a business where AI deepens an already strong moat and increases long term earnings power. OWNED

Most impacted : SEEK (SKE) not owned — no inventory exclusivity

Applying our AI disruption framework to SEEK, the structural risks are more pronounced than the near-term numbers suggest.

The structural challenge: non-exclusive inventory

SEEK operates Australia’s dominant employment marketplace with 4.9x the placement share of its nearest competitor. The near-term numbers look resilient: H1 FY26 revenue up 12%, EBITDA up 19%, guidance upgraded. But the structural foundations are deteriorating in ways the income statement does not yet reflect.

The core problem is inventory. The same job advertisement appears simultaneously on SEEK, Indeed (free to post), LinkedIn, and the employer’s own career page. A job ad is pure text — identical, freely distributable, and replicable with a copy-paste. Unlike property (a unique physical asset requiring inspection) or a car (requiring a test drive), a job listing has essentially zero platform exclusivity. SEEK itself estimates up to 70% of all online job ads appear on its platform — but nearly all of those appear elsewhere too, for free. Market dominance built on non-exclusive inventory is a different thing entirely from a structural moat.

Why AI compounds the structural challenge:

The structural threats were present before AI. AI is the accelerant. LinkedIn brings Microsoft’s full AI resources, a professional identity layer no job board can replicate, and 1 billion+ members globally. It is already the default channel for white-collar and professional hiring. AI search agents that simultaneously scan SEEK, Indeed, LinkedIn, and company career pages in seconds make platform loyalty irrelevant. The agent becomes the interface; SEEK becomes an interchangeable data feed. Employers can source candidates proactively through AI tools without posting a job ad at all and there is no regulatory floor requiring them to do otherwise.

The data disadvantage compounds this. SEEK’s dataset — job ads and application behaviour — is comparatively narrow. LinkedIn holds professional identity, career history, skills endorsements, connection graphs, and behavioural data across a billion members. In an AI-driven hiring environment, data depth increasingly determines competitive outcome and SEEK’s dataset is structurally narrower than competitors such as LinkedIn’s.

The yield strategy: correct, but not a solution:

SEEK has reorganised its pricing model intelligently, shifting toward yield-based monetisation that extracts more revenue per ad through AI-enabled premium tiers. The strategy is working in the near term and sets up ongoing yield growth. But it is a race against structural deterioration, not a solution to it. Monetising more aggressively from a shrinking or commoditising inventory base has a ceiling — and the investment required to close the AI product gap will pressure margins before it improves the competitive position.

The investment case: Not owned

The near-term earnings trajectory is not the concern — yield expansion is a real and durable lever in the medium term, and SEEK’s market position in Australia provides a meaningful runway. The concern is the investment cycle ahead. Closing the AI product gap relative to LinkedIn requires sustained R&D spend that will pressure margins at precisely the point when job ad volume growth is softening. Weak job ad volumes are already producing slight downgrades. The combination of volume pressure, rising investment requirements, and a structurally weaker data asset than the dominant global competitor creates a difficult setup for earnings growth beyond the current yield cycle.

What to watch:

Job ad volume trends are the leading indicator — not yield, which can continue growing even as structural foundations weaken. Watch for any signs of LinkedIn or AI-native hiring tools beginning to take share in the Australian market and monitor the pace of R&D investment relative to margin guidance. A guidance upgrade driven entirely by yield rather than volume improvement would warrant closer attention.

Outcome:

The name with the most pronounced AI disruption exposure in our analysis. Commodity inventory, an AI-amenable matching function, a data asset that cannot compete with LinkedIn’s professional graph, and no regulatory floor for job board usage. The yield strategy is working in the near term, though it addresses the symptoms rather than the underlying structure. NOT OWNED.

Portfolio implications

The AI disruption narrative has driven a broad derating across ASX technology and digital platform stocks — but the reality is more nuanced. AI disruption is not uniform. It plays out differently for each business depending on a variety of factors such as moat structure, data quality, inventory exclusivity, execution capability etc.

Some of the derating reflects genuine structural risk that is now better understood. In other cases, we believe the market has overreacted, creating attractive entry points in businesses where AI is not a threat but a tangible growth driver.

As AI continues to reshape competitive dynamics across sectors and industries — rapidly and in ways that were difficult to anticipate even twelve months ago — the case for reassessing each business on its own merits has rarely been stronger. Ai disruption is far from a one-size-fits-all for ASX-listed technology companies. This bottom-up analysis of AI benefits and risks to earnings power of specific businesses informs our investment process in order to identify high quality earnings leaders.