Description

Micron Technology Inc is one of the world’s largest semiconductor companies, specialising in memory. Micron’s DRAM (“Dynamic Random Access Memory”), NAND (“NOT AND”) and NOR (“NOT OR”) memory products are used in everything from computing, networking, and server applications, to mobile, embedded, consumer, automotive, and industrial designs.

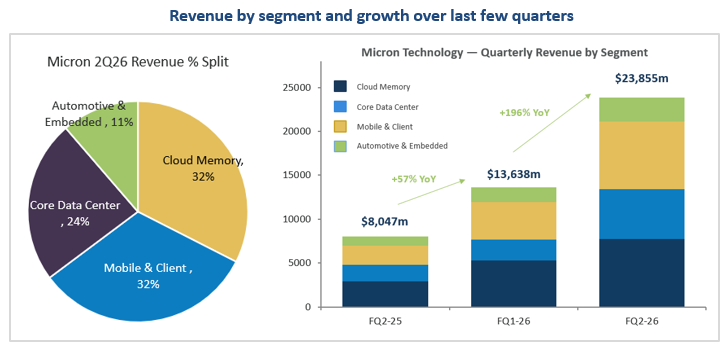

Micron is the #3 global supplier of DRAM with c25% market share, and a top 4 NAND producer. DRAM now accounts for c75% of the revenue, reflecting the company’s increasing exposure to AI-driven High Bandwidth Memory (HBM) and server memory demand.

The business is vertically integrated across R&D, wafer fabrication, components, and module assembly. Test facilities are located in Taiwan, Japan, the US, Malaysia, Singapore, India, and China with R&D facilities in Italy, Mexico, and Germany. Micron’s largest customers are cloud hyperscalers and AI infrastructure providers, alongside PC and data centre OEMs and handset makers.

Global Memory Market: The AI Supercycle

The global memory market is in the midst of a structural super cycle, which is fundamentally different from prior boom-bust episodes. Memory chips are emerging as a critical bottleneck in the global AI ecosystem, underpinning the expansion of agentic AI architectures. Currently, demand is exceptionally tight leading to extraordinary price escalations and driving an explosion in earnings across the key memory makers.

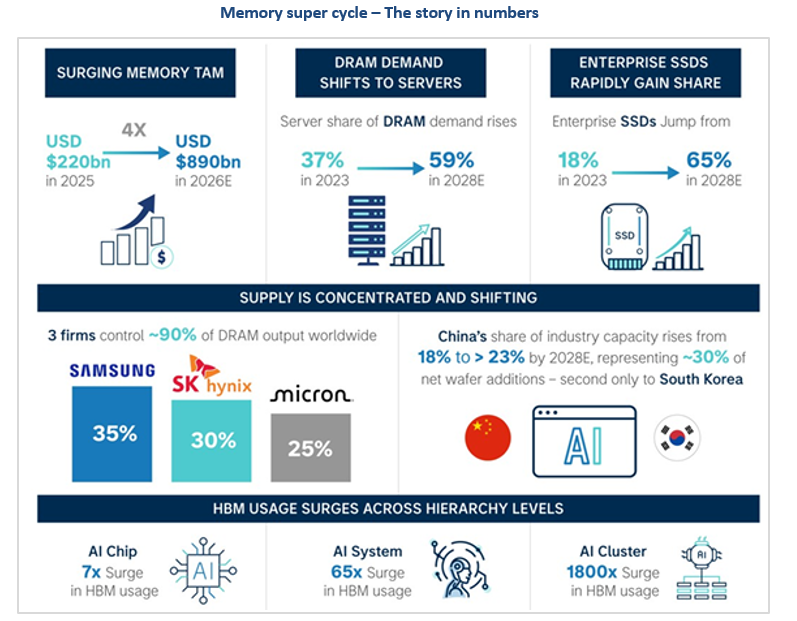

Demand – Supply Imbalance: The global memory market entered 2026 in the tightest supply-demand balance in modern history, with demand fulfilment rates are at record lows.

- AI infrastructure demand shifts wafer capacity away from consumer applications toward HBM, server DRAM, and enterprise SSDs (solid state storage drives), creating tightness across the entire memory chain.

- Samsung and SK Hynix have both warned that shortages will persist through at least 2027 while Micron’s CEO has stated that they can only fulfill 50-66% of strategic customer orders in the current environment.

- Consensus is currently anticipating that meaningful new capacity will not reach production volume until the second half of 2027 at the earliest, with the bulk arriving in 2028.

Pricing power: Companies selling into AI are currently enjoying unprecedented pricing power, while the buyers face margin pressure. In an agentic AI world, demand and pricing power gravitates towards memory and CPU plus the associated supply chains.

- Samsung, SK Hynix and Micron together control c90% of the global DRAM market and 100% of the HBM market, giving them significant pricing power.

- Memory prices rose more than 6-fold over the last year, a sharp discontinuity from the multi-decade price declines. DRAM contract prices rose 90–95% qoq in 1Q26 alone and a further 58–63% in Q226, while NAND contracts are tracking up 70–75% in 2Q26.

- The newly established structural bottleneck suggests sustained upside risks to consumer goods prices in the coming years.

Investment case

- DRAM demand fundamentals remain compelling, underpinned by Cloud and AI server workloads. Hyperscaler infrastructure spend is growing strongly driven by both the volume of data and the nature of the workloads (AI training, inference, big data). Building memory fabrication plants takes years, so there is no quick response to address the spike in demand.

- Oligopoly structure underpins pricing discipline. The DRAM market has consolidated from approximately 20 producers in 1993 to three – Samsung, SK Hynix, and Micron – with all three publicly committed to technology-led bit growth rather than wafer expansion.

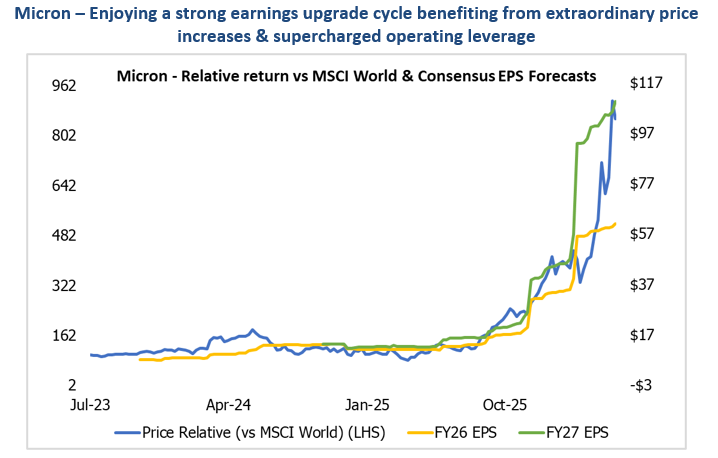

- Earnings are being materially upgraded. Micron’s FY2026 consensus EPS has moved from ~US$34 to ~US$60 as Q1 actuals from Samsung and SK Hynix revealed the magnitude of pricing moves. Unlike prior memory cycles, contracted pricing removes the spot-price volatility that historically destroyed memory company earnings.

- Software efficiency is a feature, not a risk. Efficiency gains from model quantisation and distillation reduce per-query memory needs but expand the addressable market. Alternative architectures such as CXL improve memory utilisation but complement rather than replace HBM. None of these dynamics eliminate HBM dependence before 2028 in our view.

- Valuation remains attractive. Despite the 720% rally over the last year, Micron still trades on a forward PE of <10x. Looking ahead, we expect multiple expansion to be a bigger driver of returns as investors price in a longer duration to earnings power, also supported by buybacks expected to commence in FY27.

Conclusion

Memory stocks have delivered strong returns in both 2025 and 2026, but the investment case is not exhausted. Supply remains critically tight, demand fulfilment rates are at record lows, and meaningful new capacity is not expected until the second half of 2027 at the earliest. With Micron’s consensus EPS nearly doubling in a matter of months, earnings are still seeing material upgrades. Looking ahead, the key risk to monitor is not demand, which if anything is strengthening, but the supply response: memory share prices have historically peaked 6–9 months ahead of the earnings cycle turning, so discipline around exit timing will matter as much as the entry thesis. For now, the structural bottleneck remains firmly intact, valuation is still undemanding at under 10x forward earnings, and we see the next 12 months as a compelling phase of the super cycle.