Alphinity Global – May 2026

Japan is changing — and the pace of that change is easy to underestimate from a desk in Sydney. Global Portfolio Manager Chris Willcocks recently completed a week-long investor trip through Osaka, Tokyo, Kyoto and Nagoya, meeting management teams across Industrial, Consumer, Property and Technology companies. The on-the-ground experience reinforced and deepened a thesis already forming in our portfolios. Below we share the highlights from those observations — and two quality Japanese companies which are in an earnings upgrade cycle.

Three forces reshaping Japan

Japan’s transformation rests on three structural pillars that are now compounding positively for the first time in decades. Each alone would be noteworthy; together, they represent the most significant fundamental improvement recent memory.

The End of 40 Years of Deflation

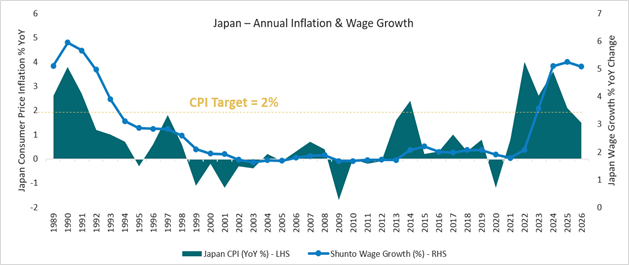

Japan has been broadly deflationary for the better part of four decades. Deflation becomes embedded in behaviour; consumers defer purchases, companies avoid price increases and wages stagnate. Japan has now sustained inflation for three consecutive years, and the behavioural shift is tangible. Rail companies are raising fares for the first time in their corporate history. Convenience stores are putting through price increases of up to 50% on select products, with minimal demand destruction. Wages are rising 5-10% at many companies and with poor demographics, job security is high.

Inflation Has Finally Arrived & Wages are Keeping Pace

Corporate Governance Reform Reaches a Tipping Point

Pressure from the Tokyo Stock Exchange to improve capital efficiency and investor returns has been building for ten years and we are now seeing the results. Several companies we met had launched their first-ever share buybacks. Cross-shareholdings are being unwound. Non-core assets are being divested — with one consumer company even selling its marriage counselling business as part of a strategic clean-up. Others were hosting their inaugural investor days. These may sound like trivial changes, but they reflect a fundamental reorientation towards minority shareholders, and most importantly, they are driving improved returns on equity.

A Populist, Pro-Growth Political Mandate

Prime Minister Takaichi has secured a strong political mandate to drive her nationalistic, pro-growth agenda. For investors, this matters because it provides policy stability and support for the economic reflation already underway.

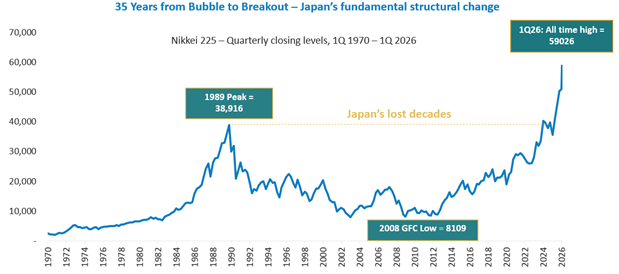

Taken together these macro forces are driving up asset prices and boosting consumer confidence. You see evidence of this across the cities and financial markets. House prices in parts of Tokyo have appreciated ~40% in six months, the Nikkei has surpassed its 1989 all-time high, inbound tourism is at record levels. There were more Ferraris and Lamborghinis on the streets of Tokyo than we have seen in any city recently. Mirroring global trends, the lower-end consumer is less buoyant, and construction faces increasing cost headwinds, but the broader picture is one of a country regaining its economic confidence.

The Japanese stock market in context

Against this macro backdrop, the question for active investors is not whether Japan is changing — it is which companies are best placed to capture that change.

Two high quality Japanese companies

Alphinity invests in Earnings Leaders — quality businesses, trading at reasonable valuations, that are entering or sustaining an earnings upgrade cycle. Japan, at this point in its structural reset, is generating exactly that kind of opportunity. The two companies we discuss below are held across our global funds.

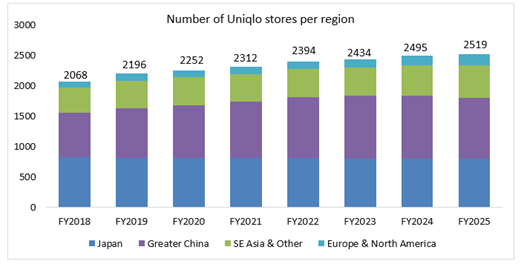

Fast Retailing — the Japanese apparel giant behind the UNIQLO brand — has quietly evolved from a domestic discount retailer into one of the world’s most compelling consumer growth stories. Founded in 1949 and listed in Tokyo since 1999, the company today generates ¥3.4 trillion in annual revenue across over 2,500 stores in more than 25 countries, with a long-term revenue target of ¥10 trillion. At the helm is founder Tadashi Yanai, who retains a ~40% stake and remains as deeply invested in the business as ever — in every sense.

A Deliberately Simple Business Model

Where brands like Zara carry over 20,000 product lines (SKUs), Uniqlo only sells 4,000 different items — and this includes multiple colour variants of the same item. This discipline sounds limiting, but it is a strategic strength. Fewer lines mean tighter inventory management, less markdown risk, and structurally higher margins. Uniqlo focuses on what might be called ‘technical basics’: quality, functional casualwear with limited fashion-season risk and a balanced offering across genders and age groups.

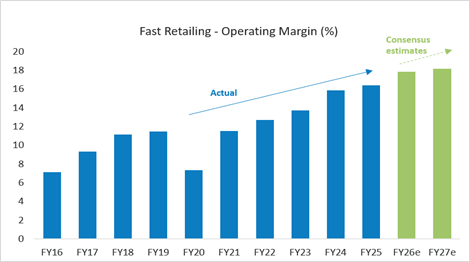

A track record of consistent margin expansion with more expected

Strong Earnings Momentum

Fast Retailing just reported second-quarter results that beat expectations on both sales and margins, across all major geographies. Revenue is growing at close to 15% per annum, driven by robust Japan same-store growth, accelerating store expansion in Europe and the US, and a recovering contribution from China.

The Market Is Underestimating the Western Opportunity

Uniqlo remains meaningfully underpenetrated in Europe and the United States relative to its footprint in Asia. We believe sell-side analysts are consistently underestimating the long-term earnings potential from this geographic expansion. Ultimately, this is a high-quality global brand in the early stages of becoming a genuine western retail force — and the market is not fully pricing that in.

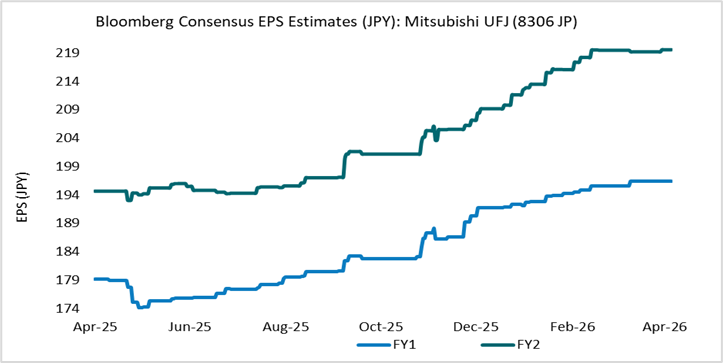

Mitsubishi UFJ Financial Group (MUFG) is Japan’s largest bank by deposits and loans, with significant operations in the US and Southeast Asia.

The Core Thesis: Rising Rates Change Everything for Japanese Banks

Japanese banks have operated in a near-zero or negative interest rate environment for over a decade. This structurally compressed net interest margins and suppressed profitability. As the Bank of Japan normalises monetary policy — which is now underway — the earnings leverage is significant. A sustained shift to positive real rates in Japan is, arguably, the single most powerful earnings tailwind available in global banking today. MUFG, as the largest Japanese bank, is a direct expression of this trade.

Quality and Diversification Often Underappreciated

MUFG generates approximately 40% of group profits outside Japan — roughly 20% from the US (excluding a stake in Morgan Stanley), 10% from Korea, and the remainder from Asia and EMEA. This geographic diversification is not always reflected in how the stock is discussed. Corporate governance has also improved substantially: the board now includes 10 non-executive directors, shareholder returns are rising, and the company has a clear target to reduce legacy equity cross-holdings.

Valuation Remains Attractive

Despite the re-rating underway, MUFG continues to trade at a modest multiple. Improving ROE, rising dividends, and a growing buyback program are catalysts for further re-rating. For advisers seeking broad Japan macro exposure with financial sector ballast, MUFG is our preferred vehicle.

MUFG – Strong earnings upgrade cycle underpinned by normalised monetary policy

Japan’s transformation has been a long time coming — and that is precisely what makes it compelling. Structural change of this magnitude does not reprice overnight. The combination of persistent inflation, genuine corporate behaviour change, and a politically-supported growth agenda creates the conditions for a multi-year earnings upgrade cycle — exactly the environment in which Alphinity’s investment approach is designed to add value. We will continue to seek opportunities as Japan’s reset deepens.