This content was originally published by Livewire on 23rd April 2026.

This interview was filmed 1st April, 2026.

Australia’s sharemarket had a strong run through February – outperforming the US, buoyed by a solid reporting season and a sharp rotation into resources stocks. But the mood has shifted since. The Iran war, sticky inflation, and consumers feeling the pinch have complicated the picture considerably.

Stuart Welch, portfolio manager at Alphinity Investment Management, sat down with Livewire to walk through how his team is thinking about Australian equities right now and why their answer to macro uncertainty is, largely, to ignore most of it – and to focus on the company earnings.

Watch the video above for all of the insights and how they are positioning for what’s next.

INTERVIEW SUMMARY

The reporting season that mattered

February’s earnings season was genuinely strong by historical standards. Welch describes the beat rate and subsequent upgrades as among “the highest that we’ve seen in recent history, putting aside some of the COVID stimulus boom.” Resources companies led the charge, continuing a trend that had been building since around mid-2024.

What’s muddied the picture for the Australian share market since is the Iran war; the risk Welch would add to the usual list of concerns like inflation, AI disruption and cost-of-living pressure, precisely because of what it’s doing to fuel prices.

“The longer the Iranian war carries on for, the more risk that it causes more damage to the global economy.”

In Australia’s case, this is particularly problematic.

“Inflation was already above the band and increasing, and that has kind of forced the RBA’s hand into actually increasing or hiking rates despite a consumer that was already softening.”

Earnings revisions are the signal

Alphinity’s approach is built on two beliefs. Earnings drive share prices, and positive earnings revisions tend to beget more positive earnings revisions.

“If a company gets one earnings increase to their forecasts, it’s likely to drive a second, third, and the fourth. And that’s the period of time that we want to be invested,” says Welch.

Welch notes that while Alphinity have made some defensive adjustments at the margin due to the potential impact of the Iran war as it continues and domestically, inflationary pressure, it hasn’t been a wholesale repositioning.

“As the macroeconomics move, we’re constantly evaluating that and changing our earnings forecasts. As it stands today, we haven’t seen a huge change in earnings leadership…but there certainly are some impacts at the margin where we are seeing.”

On the tech selloff

The rotation out of tech has been one of the dominant market stories of 2025. Welch doesn’t dismiss the AI disruption threat to software businesses, but he’s also not calling time on the sector.

“At this stage, it’s mostly been a valuation impact. And what we’ve seen is the market indiscriminately sell down the sector without a huge change in the earnings leadership within the space at this point.”

He draws a comparison to the genuine disruption in traditional print media. What initially looked like an overreaction did in fact eventually show up in earnings – and says he isn’t ruling out the same happening in tech.

As we saw with traditional print media when they came under pressure from disruption, often those challenges that the market is forecasting can manifest in earnings in the fullness of time as well.

Rather than making a large sector bet either way, Alphinity is running roughly neutral on tech, holding only a small number of companies they think are better placed to navigate whatever comes next.

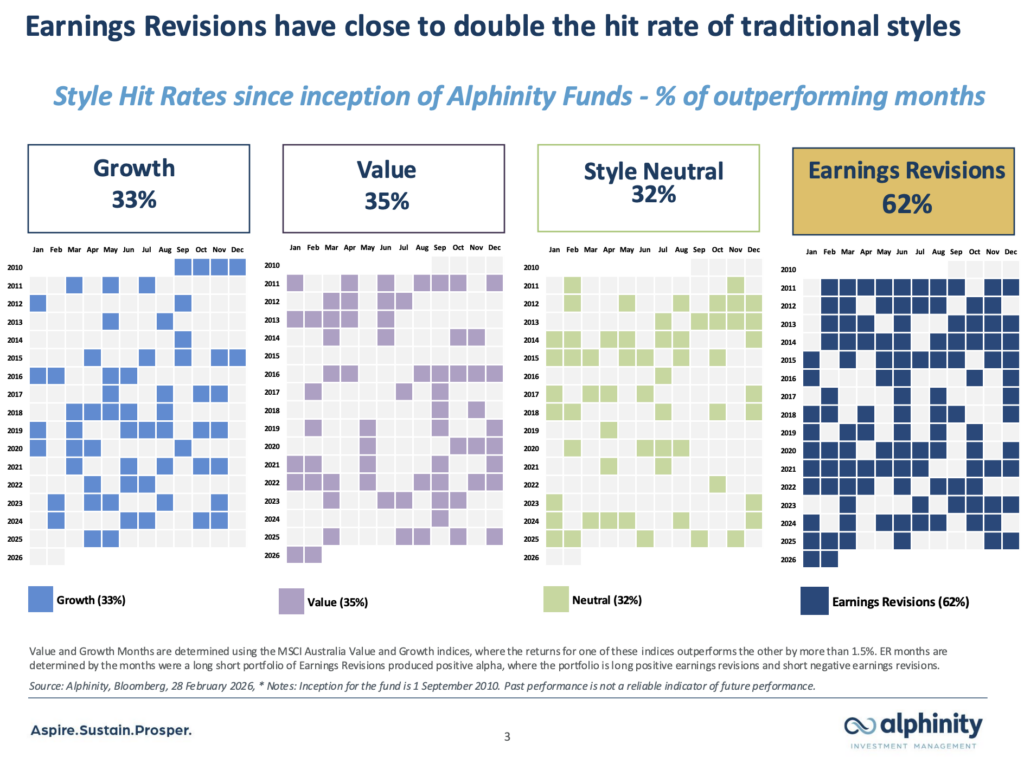

Why being style agnostic expands the opportunity set

Alphinity describes its approach as style agnostic, meaning they’re not structurally biased toward growth or value.

Since 2010, growth stocks have outperformed roughly a third of the time, value stocks a third of the time, and there’s been no clear pattern the remaining third. But companies that are getting earnings upgrades – regardless of which bucket they sit in – have outperformed around 65% of the time.

“We think that gives you a bigger opportunity set, a bigger pond to sort of fish in, but then also delivers more consistent results over time as well.”

In an expensive market, the cost of being wrong is higher.

“When the overall the entire market is expensive, as we’ve seen over the last couple of years, what it really does is increase the importance of being right in terms of being in those companies that are getting earnings upgrades,” Welch says.

What’s changed in the portfolio

Commodity positions have been trimmed after a strong run, with global growth now a bigger question mark. “We’re still overweight, but we’ve just reduced some of our positions on the commodity side of things,” Welch says.

Banks have moved closer to neutral, he says. “Over the last two years, banks have been probably the only sector that’s consistently had earnings upgrades.”

With the domestic outlook softening, Welch says they took the opportunity to reduce their position in banks and the proceeds have been redeployed into positions Welch describes as offering idiosyncratic earnings upgrade stories, regardless of the macro backdrop.

“We’ve been adding to other stocks already in the portfolio, mostly where we see good idiosyncratic earnings upgrade stories, particularly in the supermarket space, the insurance space, and then also within the telecommunication space.”