The macro has taken over. Here’s how we’re navigating it

Markets don’t wait for certainty. They reprice the expectation.

After a strong run into February 2026, led by Materials and Banks, two of the most economically sensitive corners of the Australian market, the landscape has shifted quickly. The Middle East conflict has moved markets from micro to macro almost overnight, raising a familiar and uncomfortable question: what happens to growth from here?

The short answer is that it likely slows; certainly, from what expectations were only a few months ago. The longer answer depends heavily on one man, and as anyone watching closely will attest, predicting Trump in the space of a single news cycle is ambitious, never mind longer term.

The Australian backdrop is more complicated than most

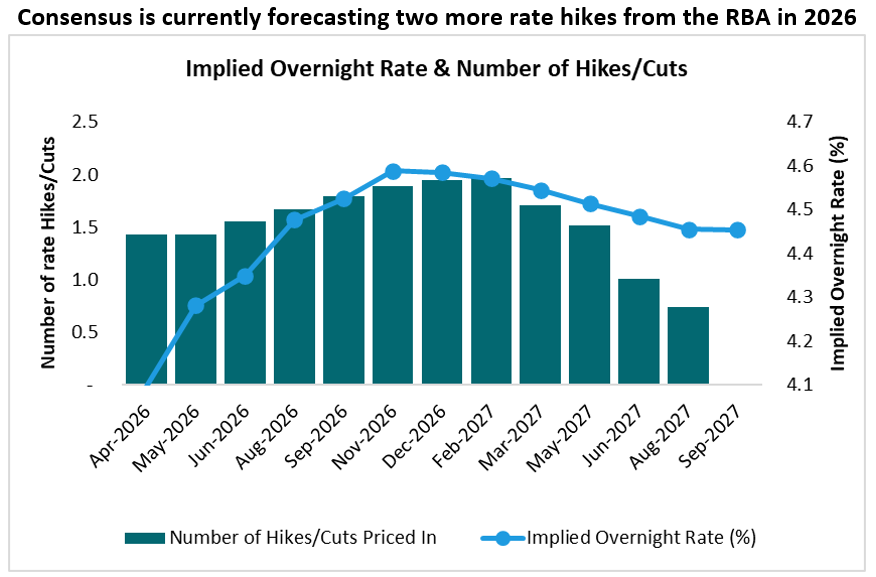

Australia entered this period with a problem most markets didn’t have to the same extent: a persistent lift in underlying inflation that had already forced the RBA’s hand. Two rate rises into a new cycle, and central bank credibility was already being tested. Consumer confidence had begun to wobble, and spending was pulling back even before the uncertainty and inflation caused by the war was a risk.

Now layer on a material rise in petrol prices, supply-side shocks across energy and key commodities, and growing uncertainty about where this end — and you have a consumer likely under genuine pressure.

The RBA finds itself in a difficult position. Raise rates further to fight inflation and you risk choking an already potentially slowing economy. Hold and you risk losing the inflation fight altogether. Neither is comfortable. This is the definition of a stagflationary environment, and the risks are starker in Australia than in many developed markets that this takes hold. The Federal Government’s budget will also play a role in dictating how much the interest rate lever will need to be pulled.

We don’t want to overstate the negatives — there is still momentum in parts of the economy, companies are on average conservatively positioned, and household balance sheets retain meaningful buffers. But slower growth is now more likely, and the risk distribution has skewed to the downside. The chance of a policy misstep has increased.

What we’re watching

Earnings. Full stop.

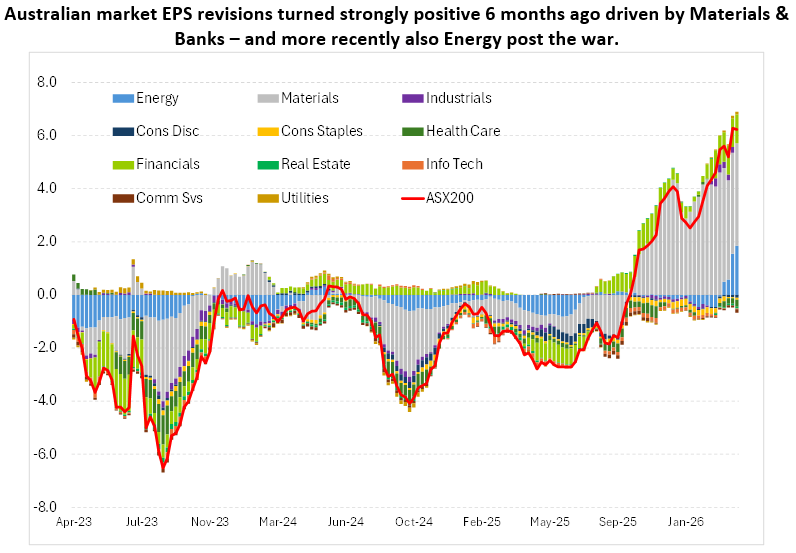

Australia had a genuinely strong six months of earnings upgrades heading into this period. That momentum is now at risk. We’re watching closely for where cost pressures and supply chain disruptions begin to feed through, particularly across the large-cap miners and banks, which have driven the bulk of recent earnings momentum.

The good news: market valuations have reset to more reasonable territory (ASX200 & ASX300 now at 17.5x PE forward vs recent highs of 20x). That cushion matters. But it disappears quickly if earnings downgrades follow. We’re not there yet, but we’re watching.

How the portfolio is positioned

With genuine uncertainty elevated, this is not the environment for bold, concentrated bets. Instead, we’ve been making deliberate, measured tilts — reducing exposure to emerging risks and adding to areas with more resilient earnings

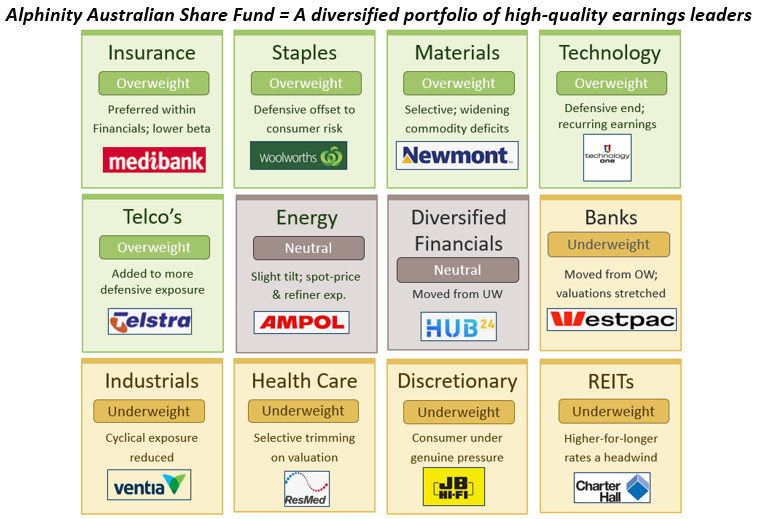

- • We’ve taken profits in global and domestic cyclicals — metals and mining, discretionary, and banks — where earnings are most exposed to an economic slowdown. In their place, we’ve added to defensive earnings streams: Staples (Woolworths), Telecommunications (Superloop, Telstra), and Insurance (Insurance Australia Group, Medibank).

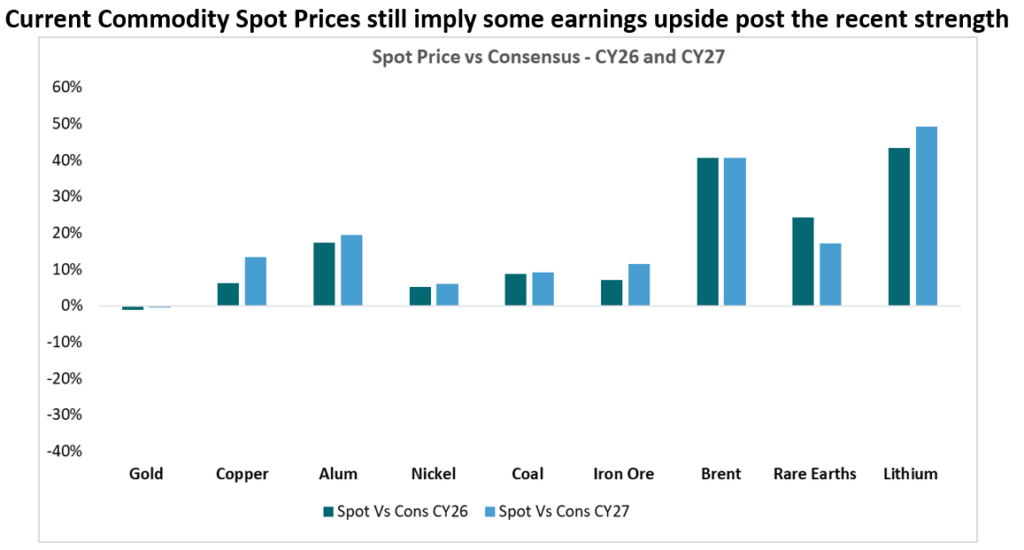

- On Energy, we remain broadly neutral but with a slight tilt toward spot-price and refiner exposure (Woodside and Ampol). Even if the conflict resolves quickly, structural damage to supply infrastructure suggests oil prices are unlikely to return to recent lows anytime soon.

- We retain a modest overweight to Metals and Mining, but well below recent highs and highly selective in where we’re positioned. Where commodity deficits have genuinely widened — aluminium being a clear example, with the supply gap widening materially since January — we see better-supported prices and potential for more earnings upgrades (Newmont, Rio Tinto, BHP, Alcoa).

- REITs remain underweight, with a preference for Charter Hall within the sector. Its high-quality portfolio and strong balance sheet provide relative insulation in a higher-for-longer rate environment relative to the broader REIT sector.

- Our Technology exposure, while modest, stays at the defensive end of the spectrum — businesses with durable, recurring earnings streams (Technology One and Life360).

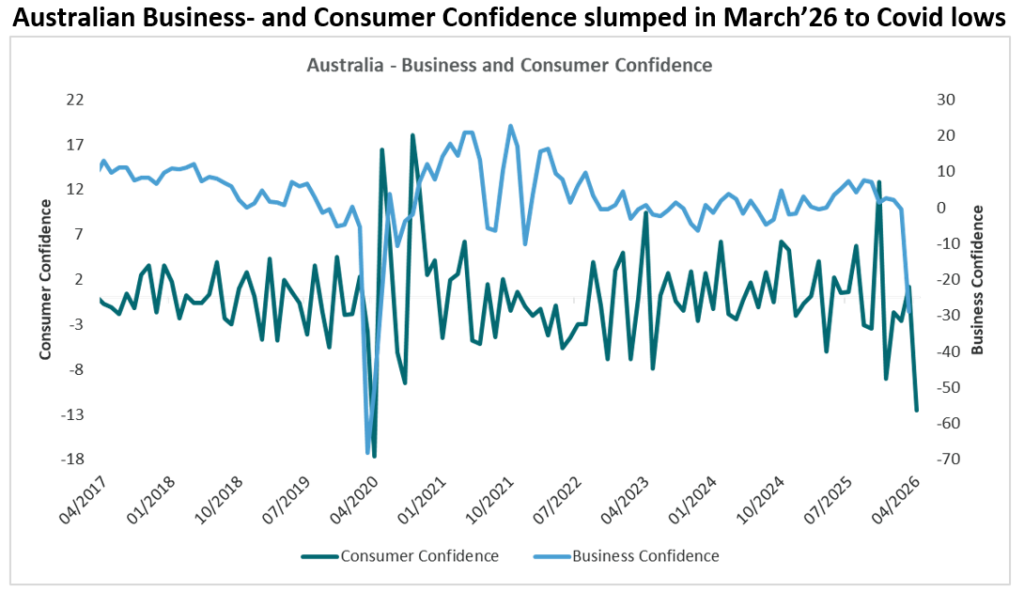

- The domestic consumer remains at risk with demand growth clearly slowing. Both Business and Consumer confidence slumped during March’26 to levels last seen during the Covid pandemic. We’re underweight the Consumer overall — more so in Discretionary, offset somewhat by an overweight in the more defensive Staples (Woolworths).

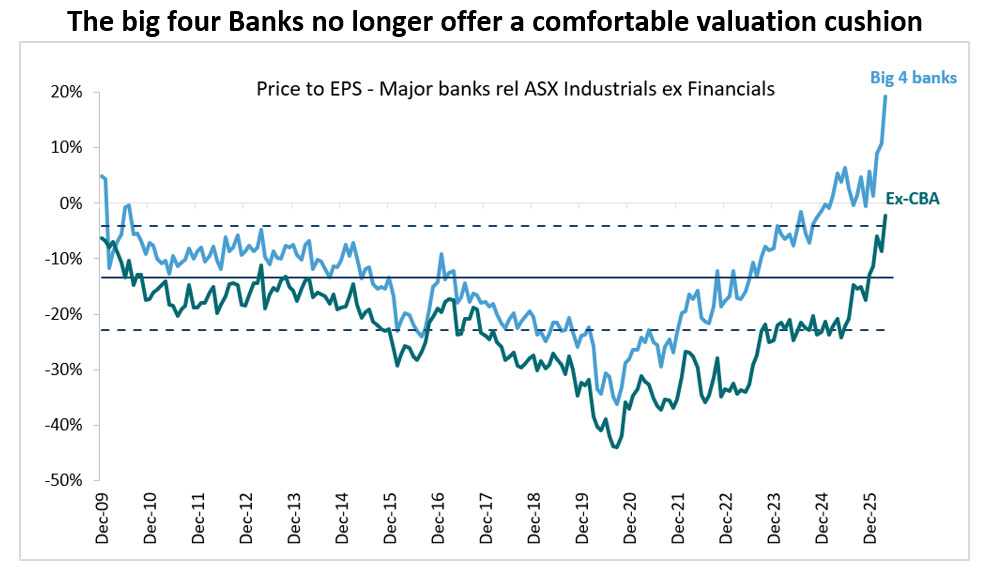

- We’ve moved to small underweight on Banks, shifting exposure a bit toward Insurance — a less beta-sensitive part of the sector. Bank valuations look stretched; ex-CBA the picture improves, but recent market moves make even a relative value argument difficult to sustain.

The bottom line

This is an autumn for patience. The macro uncertainty is real, and we won’t pretend otherwise. But uncertainty is not the same as paralysis — it’s an invitation to think carefully about where earnings are genuinely supported and where they are not.

We are tilting. Slowly, purposefully. And we will keep tilting in the direction the evidence points.

As always, we’ll let the earnings do the talking.