As we enter 2026, global equity markets are poised for the next phase of expansion. After a year defined by policy disruption, technological revolution, and geopolitical uncertainty, investors are rightly questioning whether the narrow leadership and momentum-driven returns of recent years can continue. Our view is that 2026 represents an evolution in market dynamics: from surviving tension to capitalising on expansion, from chasing narratives to backing earnings, and from speculative fervour to quality compounding. If 2025 was the year of “Tariffs, Tech, and Tension,” we believe 2026 will be remembered as the year of “Earnings, Expansion, and Excellence.

Reflecting on 2025: Tariffs, Tech, Tension

Last year’s market narrative was dominated by three powerful forces. Trump’s return to the White House brought immediate focus back to trade policy, creating uncertainty for global supply chains, though corporate earnings ultimately proved resilient. AI infrastructure spending remained the dominant growth narrative, with hyperscalers committing over $200 billion in capex and creating a halo effect across the value chain from semiconductors to power infrastructure. Meanwhile, geopolitical tensions—from ongoing conflicts to monetary policy pivots—kept risk premiums elevated, yet markets demonstrated remarkable resilience with relatively shallow corrections.

Judging by the opening weeks of 2026, elements of these three T’s appear determined to follow us into the new year. Investors should remember last year’s lesson: even in strong years, significant volatility is inevitable. The key is maintaining discipline through the swings rather than reacting to them.

2026 Outlook: Earnings, Expansion, Excellence

EARNINGS: A Constructive Global Cycle Broadens

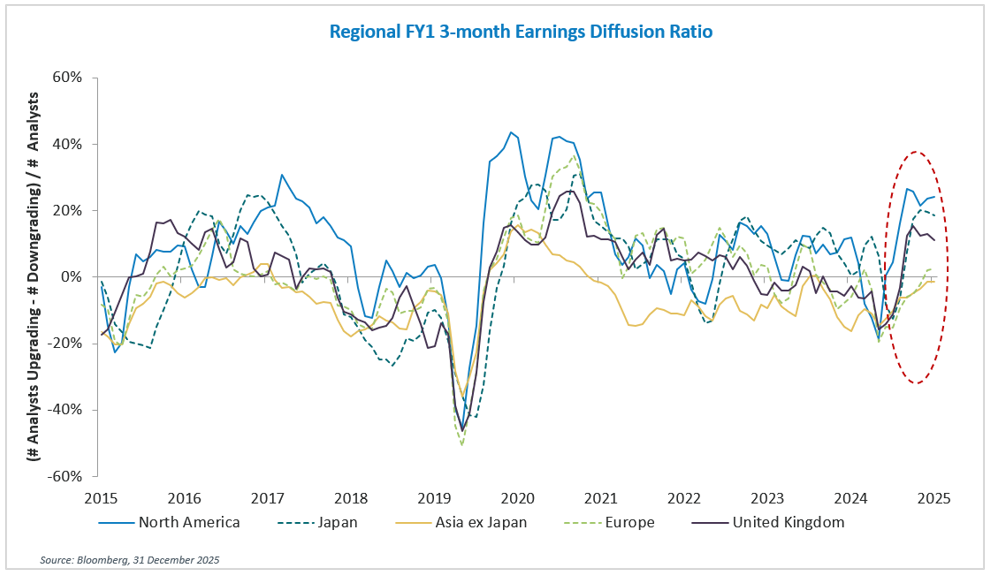

The global earnings cycle is exhibiting encouraging breadth and momentum after an extended period of narrow leadership. Earnings revisions are turning positive across regions, with upgrade ratios improving and the percentage of companies seeing earnings upgrades expanding well beyond the mega-cap tech cohort that dominated recent years.

Earnings sentiment (diffusion ratio) at a 4-year high with a positive inflection across major regions

Note: Earnings diffusion ratio = the number of earnings upgrades/downgrades

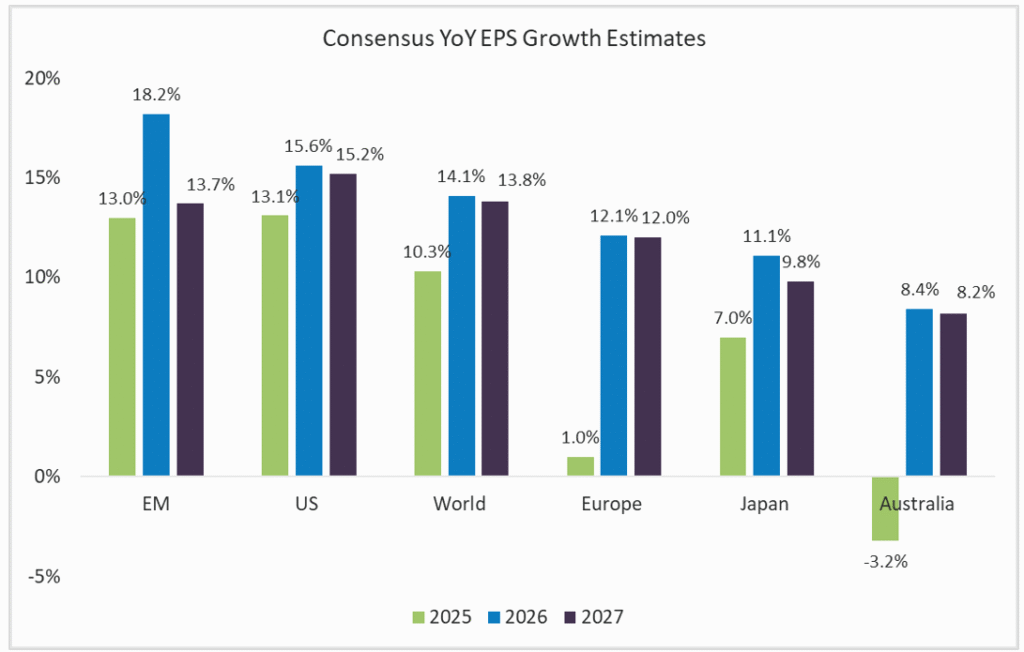

Technology and Financials continue to lead earnings growth revisions, though they have recently been joined by Materials as higher commodity prices flow through to corporate results. Healthcare, Industrials, and Consumer sectors still lag but are showing signs of stabilisation. Consensus now expects the MSCI World index to deliver healthy double-digit EPS growth of approximately 14.1% in 2026 and 13.8% in 2027. Most major markets are projected to see a rebound in earnings growth over this period, with current laggards like China and Europe positioned to catch up. This broadening earnings picture supports higher equity valuations and reduces the concentration risk that has concerned many investors.

Early signs from the 4Q25 reporting season suggest the earnings trajectory remains strong, though market reactions are more subdued as elevated valuations raise the bar for positive surprises. If companies deliver the usual 4-5% beat, this will mark a fifth straight quarter of double-digit earnings growth—a streak not seen since late 2018.

Consensus expects strong earnings growth across all key regions in 2026 and 2027

We remain relatively constructive on the outlook for corporate earnings in 2026, which we expect to be supported by generally favourable macroeconomic conditions. Importantly, these supportive conditions are not dependent on a single driver but reflect expansion across multiple fronts.

EXPANSION: Multiple Tailwinds Converge

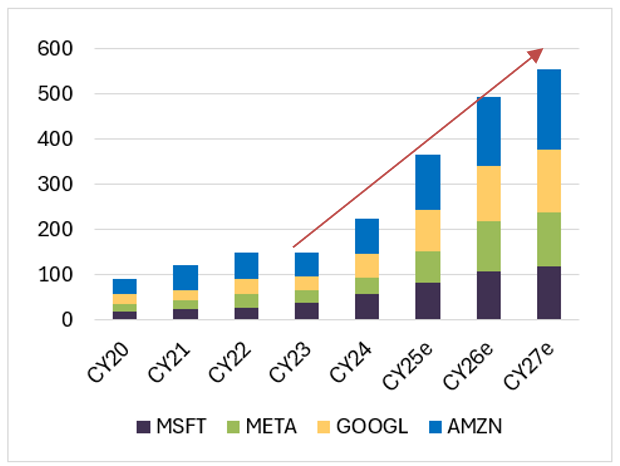

The macro backdrop appears constructive across multiple dimensions. Economic growth remains positive, inflation is under control, credit spreads are tight, and both fiscal and monetary policy provide stimulus. The AI capex cycle represents a multi-year growth driver still in early innings, with annual hyperscaler spending expected to exceed $400 billion flowing through to semiconductor manufacturers, data centre infrastructure providers, power utilities, and enterprise software companies. This sustained investment pulse operates largely independent of traditional business cycles, providing a reliable growth anchor for the technology ecosystem.

Hyperscaler capex intentions (US$bn) – On track to $500bn in 2026

Consumer fundamentals remain surprisingly robust despite increasing bifurcation. Unemployment sits near historic lows across developed markets, real wage growth persists, and household balance sheets are healthy following pandemic-era deleveraging. The emerging K-shaped pattern—with upper-income households benefiting from wealth effects while lower-income consumers face pressure—creates divergent retail dynamics but hasn’t derailed aggregate spending. With consumption representing 70% of US GDP, this resilience provides a critical foundation for corporate earnings.

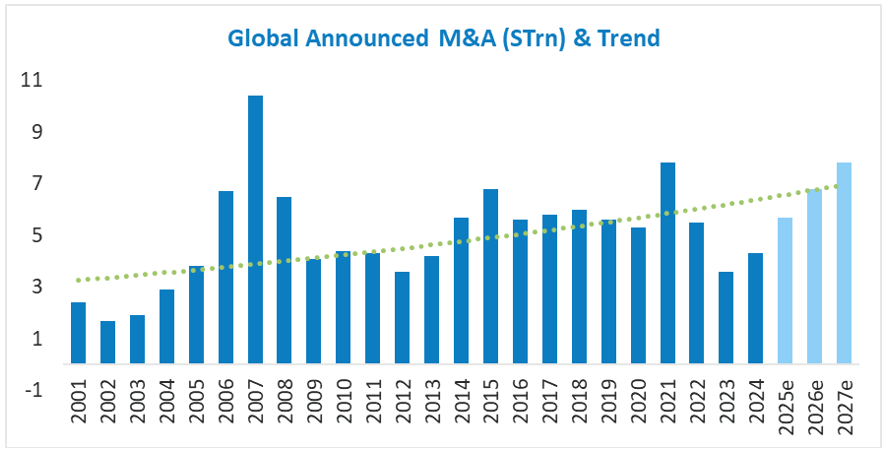

Mergers and acquisitions rebounded sharply in 2025 after hitting 20-year lows in 2023. The catalysts driving this resurgence, lower rates, open capital markets, improving corporate confidence, and more favourable regulation, remain firmly in place. Companies are no longer waiting on the sidelines as they pursue growth and technology capabilities through strategic transactions. Deal activity is forecasted to reach $6.8 trillion in 2026 and $7.8 trillion in 2027*, supported by private markets industry sitting on $4.2 trillion of dry powder (approximately $8 trillion of buying power with leverage), the stage is set for sustained M&A momentum. Across our portfolios, serial acquirers like Amphenol, Parker Hannifin, Motorola Solutions, and CRH continued adding value through disciplined consolidation strategies, while investment banks JPMorgan and Morgan Stanley benefit from elevated advisory and underwriting activity.

M&A is back and broadening out

EXCELLENCE: Quality’s Overdue Mean Reversion

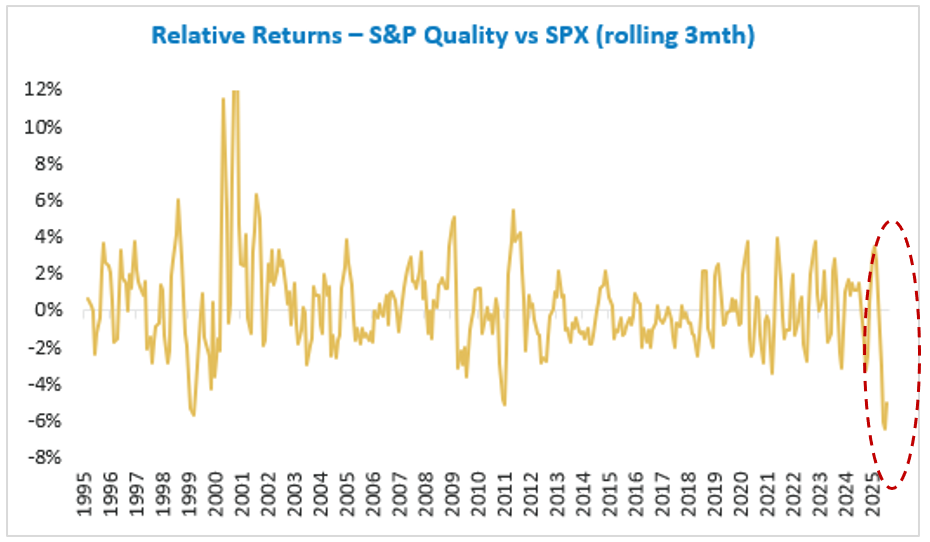

Quality as a factor has significantly underperformed over the past 18-24 months, left behind as markets chased momentum, AI narratives, and speculative growth-at-any-price stories. The “risk-on” environment favoured leverage and operational gearing over balance sheet strength, with investors willing to overlook fundamental weaknesses for revenue growth. Mega-cap tech concentration meant AI exposure mattered more than traditional quality metrics like high ROE, low debt, and stable earnings.

Sector dynamics compounded the challenge. Quality indices traditionally overweight Consumer Staples and Healthcare—both facing significant idiosyncratic headwinds—while underweighting Banks, which strongly outperformed. Elevated valuations, particularly in Europe, and speculative retail activity added further pressure. AI disruption concerns also weighed on Software, Diversified Financials, and Business Services, all typical quality portfolio constituents.

However, conditions now favour mean reversion. Relative valuations between quality and lower-quality stocks have normalized. Sector-specific headwinds are easing. Most importantly, as geopolitical and policy volatility persists, investors are increasingly valuing downside protection. Quality companies—those with sustainable competitive advantages, pricing power, and capable management teams with proven capital allocation track records—are better positioned to navigate uncertainty and deliver consistent returns. In an environment where fundamental differentiation matters again, excellence in business quality should separate winners from pretenders.

Quality as a factor had its worst year in decades during 2025

Positioning for 2026

Our portfolios are positioned to capture the broadening earnings leadership while maintaining rigorous quality standards. We combine exposure to secular growth trends—particularly AI infrastructure and healthcare innovation—with established leaders in Financials, select Industrials, and defensive Consumer franchises. The unifying theme is earnings visibility supported by competitive advantages, pricing power, and superior management teams.

AI and Technology: We maintain selective exposure across the value chain, balancing opportunity with execution risk. Our Magnificent Seven exposure include Nvidia and Microsoft for their AI leadership and supportive valuations. Beyond mega-cap tech, TSMC offers dominant semiconductor positioning with fortress balance sheet strength, Tencent combines gaming and cloud growth with exceptional cash generation, and Amphenol provides mission-critical connectivity solutions with high switching costs. We remain thoughtful about position sizes given the technology’s rapid evolution, uncertain ROI timelines for hyperscalers, and disruption risks to incumbent business models.

Financials: Global banks represent our primary cyclical exposure, benefiting from sustained net interest margins, robust capital return programs, and improving loan growth. JPMorgan and Morgan Stanley provide diversified financial services leadership, while NatWest and Caixa Bank offer compelling regional banking franchises in the UK and Spain respectively.

Healthcare, Industrials, and Quality Defensives: Boston Scientific and AstraZeneca deliver healthcare exposure through innovation pipelines and R&D productivity. Caterpillar captures industrial recovery with pricing power and durable service revenue. Defensive positions in Coca Cola and L’Oreal (Consumer Staples) offer global scale and solid organic growth. Cyclicals such as CBRE (Real Estate) and CRH (Materials) provide quality characteristics and established competitive moats.

This positioning reflects our conviction that 2026 favours portfolios combining secular growth exposure with business quality—companies that can compound earnings through volatility rather than merely benefit from beta.

A diversified portfolio of earnings leaders

Conclusion

The transition from 2025’s Tariffs, Tech, and Tension to 2026’s Earnings, Expansion, and Excellence represents more than clever alliteration—it reflects our conviction that market leadership is evolving toward a more sustainable foundation. The broadening earnings cycle, supportive macro tailwinds, and quality’s likely mean reversion create an environment where active management focused on business fundamentals should generate alpha.

The “free money” period for low-quality momentum plays appears to be ending. While volatility and policy uncertainty will undoubtedly persist, portfolios that combine exposure to secular growth trends with an emphasis on earnings certainty, balance sheet strength, and management excellence are well-positioned to deliver superior risk-adjusted returns. For investors willing to look beyond the narrow leadership that dominated recent years, 2026 offers compelling opportunities across a broadening set of quality businesses with genuine earnings power.