With so much attention fixed on the global SaaS sell-off, it would be easy to miss what actually happened in Australia in February. This was one of the strongest reporting seasons in two decades — and for those positioned on the right side of earnings, it was a genuinely rewarding period.

The Big Picture

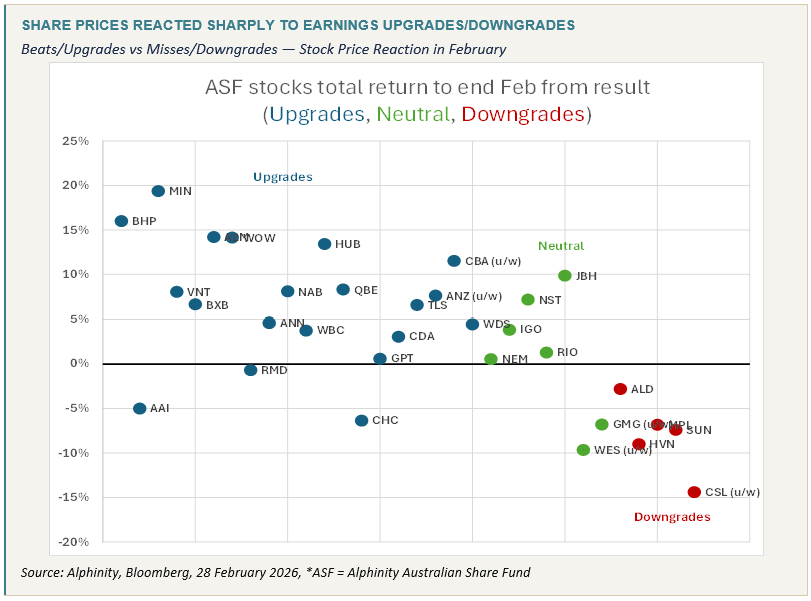

Volatility does not mean bad. It means difficult — particularly if you are on the wrong side of earnings. February 2026 was undeniably volatile, but it was volatile in the right direction: stocks moved materially in line with their earnings outcomes. Companies that beat saw their prices rise. Companies that missed were punished — and punished hard. That asymmetry, where misses drew a greater reaction than beats attracted reward, has become increasingly typical of modern markets.

Stripping away the noise, this reporting season delivered one of the highest rates of net earnings per share (EPS) beats and positive revisions seen in twenty years. Earnings went up. The market went up. Valuations were supported — and in many cases were further re-rated by the confidence that sustained upgrades generate.

Importantly, beats were driven more by margin improvement — disciplined cost management and operational leverage — than by revenue outperformance. This speaks to the quality of the earnings cycle: companies are not simply chasing the top line, they are converting it efficiently.

Earnings momentum is a real thing. Those that have ignored the consistent upgrade cycle in Banks and Materials over the past 18 months have now missed that same momentum for a third consecutive period. Where earnings were going up before, they went up again in February. Consistency compounds.

Key Themes

- Banks — persistent outperformance. All four major banks beat expectations and received earnings upgrades. A supportive domestic macro backdrop — positive volume growth, strong credit quality, resilient margins — combined with self-help stories at ANZ and WBC drove a third consecutive period of upgrades. With interest rates rising modestly and employment remaining strong, it is difficult to see what disrupts this earnings momentum in the near term. Valuation, outside of CBA, remains defensible.

- Materials — the upgrade cycle broadens. Commodity spot prices — particularly Copper and Aluminium — remain above consensus expectations, driving continued upgrades across the sector. Financial flows are providing additional tailwinds in Lithium, Rare Earths and Gold. Iron ore is more muted, with all eyes on Chinese demand signals post Chinese New Year. Earnings upside still underpins our overweight, though we have trimmed selectively as valuations have stretched.

- Large cap led, small cap lagged. The ASX 300 equal-weighted index underperformed the benchmark-weighted index by 6.8% in February — a stark divergence illustrating how concentrated strength was in large caps. Healthcare was a notable exception in the wrong direction: CSL, COH and PME all received earnings downgrades and materially underperformed.

- AI — an unavoidable reckoning for ‘Growth’ stocks. AI disruption is no longer a distant hypothesis. Cost efficiencies and headcount reductions are arriving faster than expected — WiseTech (WTC) and Block (XYZ) both announced material staff reductions in 2026. With many technology and SaaS companies on elevated valuations, the prospect of lower terminal values drove significant de-ratings, even for companies with solid near-term results.

- Consumer discretionary — caution warranted. Despite reasonably solid results, the sector was a weak performer. Margin pressures and the anticipation of further RBA rate hikes are weighing on the outlook for lower-income cohorts in particular. A strengthening Australian dollar adds further headwind for offshore earners as the RBA diverges from the Fed’s rate path.

- Capital management — a confidence signal. Twenty-two new or extended buybacks were announced during the period, signalling strong cash generation and forward confidence from management teams — a constructive underpinning for the market.

How Alphinity Portfolios Performed

It is fair to say this was one of our better reporting seasons. Our hit rate — measured by earnings beats and in-line results across portfolio overweight positions — was 85%. In our top 10 holdings, every position either beat or met expectations; 80% received forward earnings upgrades, with the remaining 20% holding flat.

Avoiding the ‘landmines’ proved as valuable as picking the winners. We were underweight or avoided CSL, COH, PME, SEK, REA, CAR, WOR, COL and QAN — all of which experienced earnings downgrades. On the flip side, the SaaS sell-off created some noise around positions in 360, TNE and HUB early in the period — but all three delivered genuinely positive results or trading updates which tempered the share price impact.

In aggregate, and in a period that produced one of the strongest upgrade environments in years, our portfolio’s revision profile was materially better than the market — continuing a trend now in its 16th consecutive year.

Three Results That Stood Out

Three holdings delivered among the most significant earnings upgrades of the season, each reflecting a core element of the Alphinity investment philosophy: identifying companies where earnings are accelerating and the upgrade cycle has further to run.

A2M delivered one of the standout results of the reporting season — a genuine beat at both the top and bottom line, with forward earnings estimates revised materially higher. The result reinforces a thesis building momentum for several periods: A2M is a structural share gainer in the Chinese infant milk formula (IMF) market, and that dynamic is accelerating despite a structurally declining birth rate environment.

The key insight is that A2M does not need a larger market to grow — it needs a weaker competitive set. Feihe continues to lose share on pricing and inventory discipline issues; Nestlé/Wyeth are under significant pressure with an estimated 15%+ revenue decline. A2M’s A1-free protein story, New Zealand provenance, and premium positioning are increasingly compelling to Chinese parents who prioritise trust and ingredient integrity above price. Expansion into lower-tier cities represents meaningful white space, largely untapped.

Near-term, the customs clearance disruption from the ARA screening blowout is temporary and isolated. Inventory levels at key channels (Sam’s Club, Herma) remained supported, and the resolution timeline is tracking in line with management guidance. The Genesis HMO product — while early stage — is growing faster than the core range with better distributor margin economics.

A2M is the clearest example in the portfolio of a company where the earnings upgrade cycle is being driven by genuine market share capture, not macro tailwinds. The combination of brand strength, channel expansion and a recovering stage 1 segment gives us confidence in the durability of the upgrade pathway. We remain overweight.

BHP’s result was a reflection of a commodity price environment that continues to surprise consensus to the upside — particularly in Copper and Aluminium. For the first time copper has topped the earnings mix, contributing the largest share of group earnings at 51% of underlying EBITDA. Spot prices have remained structurally above the levels embedded in analyst models, and with limited near-term supply response, that gap is proving persistent. Operational performance was solid, costs were in line, and the forward earnings revision was meaningful.

The China question looms large — demand signals following Chinese New Year and the detail of the 14th Five Year Plan will be watched closely. Our current read is that the structural case for Copper (energy transition, AI data centre build-out) remains intact regardless of the short-term China cycle, and BHP’s scale and asset quality provides appropriate leverage to that theme without undue execution risk.

We have taken some profit as materials valuations have stretched toward ‘expensive momentum’ territory but maintain an overweight. Earnings upside from commodity prices above consensus continues to underpin the position. The earnings upgrade cycle in Materials, like Banks, has now run for multiple periods — and it continued in February. We see no fundamental reason for that to reverse imminently.

Looking Ahead

February 2026 demonstrated something important: in a market that feels volatile and difficult to navigate, earnings remain the most reliable compass. Where earnings beat, stocks went up. Where earnings missed, stocks fell — and fell hard. The market is not broken; it is, if anything, more efficient at repricing earnings surprises than it has historically been.

For those focused on identifying companies at the early stages of earnings upgrade cycles — and disciplined enough to avoid those where earnings risk is elevated — this remains an environment where stock selection can generate genuine alpha. The 16-year track record of outperforming the market on earnings revisions is not a coincidence; it is the output of a disciplined, repeatable process applied consistently through many different market regimes.

The themes that drove February — Banks, Materials, selective large cap — are not finished. And the themes that hurt in February — elevated-valuation growth stocks, AI disruption uncertainty, consumer margin pressure — are unlikely to resolve quickly. We enter the next period with clear conviction on both sides of that ledger.