There are 3 important criteria for identifying a once in a generation buying opportunity: 1) confidence that the business model will still be viable in a generation; 2) confidence that the stock has moved out of an earnings downgrade cycle into an earnings upgrade cycle; and 3) valuation support that signals a true buying opportunity, not an opportunity to catch a falling knife.

Global equity markets have pulled back sharply in 2022 and it may be tempting to view some previously high-flying stocks as once in a generation buying opportunities. However, caution is needed because many of the worst preforming stocks year to date do not meet the 3 criteria outlined above.

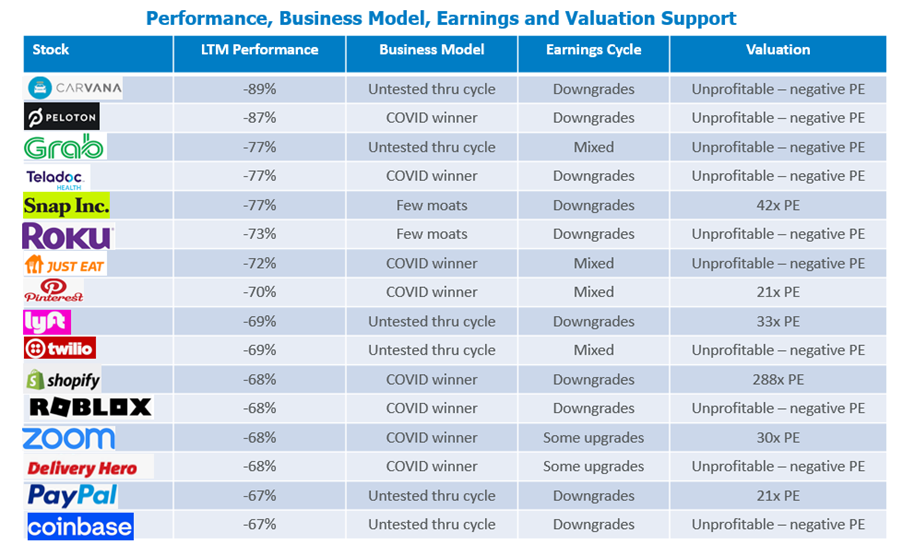

The following table shows stocks in the MSCI World Index that are down 65% or more in the last 12 months. Arguably, the vast majority of these do not meet the first criteria of a durable business model that will definitely be around for generations to come. In addition, most of these stocks are not in an earnings upgrade cycle, nor do they have strong valuation support even at these levels.

Caveat emptor for these types of stocks

Source: Bloomberg, 31 May 2022, Alphinity

Unlike the stocks in the table above, ASML is a high-quality stock that has corrected over 30% from its late 2021 high and meets the criteria of a durable business model, earnings upgrades and valuation support.

A Business Model with Staying Power

ASML is definitely going to be around in a generation as evidence by the fact that the stock listed in 1995 and has seen a few cycles already. ASML’s enviable market share of around 70% provides confidence that there are deep moats around the business that can outlast periods of strong competition or disruption.

Looking forward, ASML management likes to talk about the 3 main drivers of their stock being structural (AI, Internet of Things, 5G, Electric Vehicles, etc), cyclical (semi shortages and ongoing semi supply chain disruptions) and geopolitical (reshoring of semi capacity to the US and potentially Europe to reduce the risks associated with China/Taiwan). The combination of these 3 drivers is very powerful and supports a strong long term business case for ASML.

Earnings Upgrade Cycle

ASML’s 1Q22 result came out slightly ahead while guidance for the FY22 maintained top line growth of ~20% and strong gross margins of ~52%. The bigger earnings story from the recent Capital Markets Day was a substantial upgrade to capacity targets for FY25 based on very strong demand. The potential upgrades here are significant – in the order of +50% revenue potential over the medium term.

Valuation Support

ASML is currently trading on a PE of less than 30x versus almost 50x PE at the end of FY21. This valuation is now below its 5 year average PE and represents an attractive PEG ratio of just over 1x. Furthermore, ASML’s net cash balance sheet, 65% ROE and strong Free-Cash-Flow yield provide confidence in downside support for the stock.

As shown in the table below, ASML’s valuation support is in sharp contrast to many of the unprofitable or barely profitable tech stocks with no valuation support even at these levels. If markets continue to trend down, then many of the stocks that have been crushed in the last 12 months can continue to fall further.

Conclusion

Stick with high quality stocks with durable business models, earnings leadership and valuation support. In this context, ASML looks very attractive. Happy hunting for once in a generation buying opportunities!