Since Chat GPT3 crashed onto the scene at the end of 2022, the world has been swept up in (generative) Artificial Intelligence (AI) euphoria. AI related stocks have all rallied, companies have expanded their capital plans and gone to great lengths to explain how and why they use AI, and analysts have sharpened their bull case scenarios for future growth opportunities.

We’ve seen similar transformative technology breakthrough exuberance rise and fall in the past, such as Web 3, the metaverse and crypto architecture last year. Is AI just another tech bubble about to implode? Or something much more substantive? The answer is yes to both.

In this note, we expand on why we remain excited about the use cases and subsequent earnings potential that can be built off the back of AI in the future and why we believe this technology shift, and the value that it can create, is real. Investors however need to be very selective as the monetisation potential of AI will flow through different elements of the chain at various levels an at different times. Two clear early winners in our view are Microsoft and Nvidia.

The AI induced rally

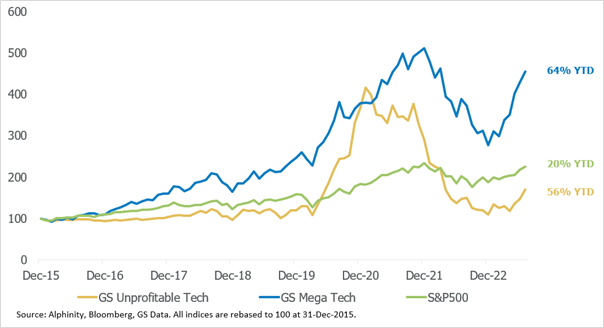

The release of Chat GPT did bring the technology sector heavily back into focus in the first half of the year with the Mega (or profitable) Tech index rallying 64% to the end of July. But this reborn tech euphoria also dragged the Unprofitable Tech stocks 37% higher, to outperform the broader US market by more than 40% and 15% respectively.

AI enthused rally has boosted profitable and unprofitable tech stocks YTD

There is undoubtedly an element of AI froth that has come into the technology sector, as some companies have seen AI potential wash into their share prices before a clear articulation of how the earnings that will back these valuations will emerge. And we have seen the downside of this where companies such as Data Dog and Palantir have had solid falls after earnings disappointments, while some of the air has also come out of other companies such as MongoDB, Snowflake and Salesforce.

We expect the market to become more discerning in terms of wanting to see a clearer monetisation path to determine who the key winners will be as opposed to the broad lifting of almost all boats even tangentially brushing up against the AI theme that we have seen so far this year.

Use cases of generative AI

In terms of winners in the AI space, it is all about a clear identification of use cases. AI is not a new theme. The difference now is generative AI developments expand these technological capabilities and put them within the reach of hundreds of millions of new users each month. The IDC estimates the global AI market will see 19% compound annual growth between now and 2026 to reach US$900bn while Goldman Sachs predicts generative AI alone could drive 7% or an almost $7trn increase in annual global GDP growth over the coming decade.

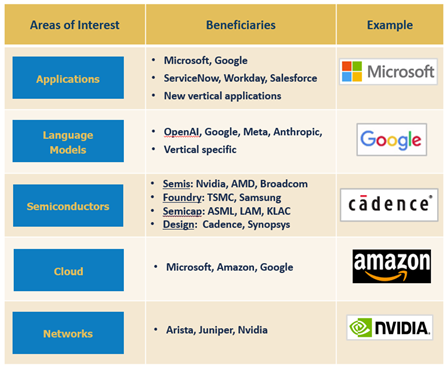

There are various elements of the tech ecosystem where value will emerge to varying degrees. At the front end you have the key enablers such as semiconductor designers like Nvidia that will benefit along with foundry businesses like TSMC and Samsung and the semiconductor equipment players such as ASML, Applied Materials and Lam Research who supply them. Then you shift towards the infrastructure names such as networks businesses like Arista, and the cloud players that span Microsofts Azure, Amazons AWS and Googles GCP.

But the really exciting opportunities should emerge beyond the initial enablers and infrastructure players and be in those businesses that can create applications based on AI. Established businesses such as ServiceNow, Workday and Salesforce are working to embed AI within their current offering, but the real opportunity is likely to be in the emergence of a business that applies AI to a deep revenue pool and owns that vertical. Whether that be in healthcare, finance or customer service, there is potential for an AI leader to emerge that could be the next big tech name in 5yrs.

AI offers a plethora of investment opportunities, but not all created equal

Source: Alphinity, 31 July 2023

Two clear early winners currently – Microsoft & Nvidia

Investing in AI is like investing in any other idea for Alphinity; find the investment ideas that are showing earnings leadership, come wrapped in a quality business, and are bound by a reasonable valuation. In AI it comes down to identifying a tangible use case and the monetisation potential that flows off the back of this to driving earnings outperformance, exceptional returns and valuation upside. Microsoft and Nvidia are two clear early winners in AI that display these characteristics.

Microsoft (MSFT) – Well positioned for broad secular trends in technology and a leader in AI

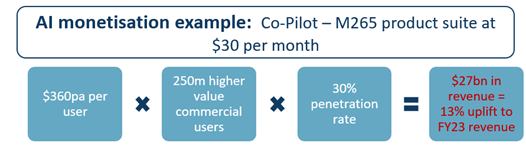

Microsoft has multiple legs of opportunity flowing from AI. At the front end, it has announced pricing for its AI infused M365 co-pilot product at $30per user per month. Applying this pricing to Microsoft’s 250m commercial users of it’s higher value products, we estimate Co-pilot can drive an extra $27bn in revenue, or 13%, over a 3-5yr period, assuming a conservative 30% penetration rate. There is also the uplift in consumption that will run through Microsofts cloud business Azure, a potentially simpler Ai product for the extra 200m commercial users on simple product sets, plus incremental gains from any shift in search traffic from Google to Bing.

Wrap this together and while the Microsoft share price has risen in 1H23, investors are currently paying 30x Price to Earnings for a business that can grow mid-teens over the next 3 with multiple growth drivers.

MSFT offers tangible AI monetisation

Source: Alphinity, Bloomberg, 31 July 2023

Nvidia (NVDA) – Global leader in Graphics Processing Units with generative AI a gamechanger

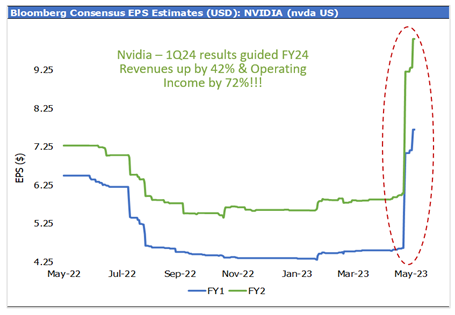

Nvidia is the other key initial beneficiary from AI, with their most recent result generating an almost unprecedented upgrade in earnings expectations for a business of its scale. Generative Ai is all about GPU’s given their ability to run calculations and simulations in parallel; the key tasks for AI. And Nvidia sits front and centre as the leader in terms of GPU performance coupled with a powerful software capability making their GPU’s flexible and programmable.

The key to the Nvidia investment case is ensuring that the current demand is not just a flash in the pan. To our mind, there is sustainability to this demand given that generative AI has triggered a shift in data centre infrastructure from CPU’s towards GPU’s. With around $1tr of datacentre infrastructure installed, and this infrastructure turning over around every 4 years, this provides rich structural tailwinds that should drive Nvidia earnings for years to come.

On our estimates, NVDA should generate around $30bn in datacentre revenue this year (2/3rds of total revenue). If we push the shift from CPU to GPU through our discounted cashflow model, we estimate that datacentre revenues can increase to $80bn CY27. Investors are paying c40x FY24 Price/Earnings, with what looks like growth to come for the years ahead.

Revenue & margin uplifts driving unprecedented EPS upgrades over next two years

Source: Alphinity, Bloomberg, 31 July 2023

In summary, AI is an exciting investment opportunity, with many growth tangents still to be discovered. But like any investment, investors need to be able to have a line of sight to the earnings potential and be disciplined in terms of what they pay for these companies to ensure that they are not riding a bubble that may eventually pop.

Authors: Elfreda Jonker, Client Portfolio Manager & Investment Specialist and Trent Masters, Global Portfolio Manager