In the world of business, there are ‘price makers’ and ‘price takers’. Companies that have pricing power from strong market positions in good industries, with wide competitive moats and high profit margins. And those that don’t.

In a rising inflationary environment, the price makers are in the pound seats, passing on higher costs and maintaining or even improving their margins. In this note we reflect on recent pricing trends and expand on two compelling price makers in our global portfolios that we expect to remain earnings leaders even as the world returns to a new normal.

Cost inflation is a key challenge, with pressures likely to persist into 2022

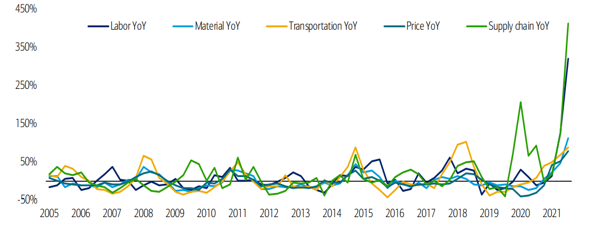

Margin pressures due to stretched supply chains, labour shortages, and higher-priced commodities have been a dominant topic this year, with mentions of “inflation” on recent earnings calls rising to a record high (see chart below).

S&P500 companies mentions of inflation related words on earnings calls (2Q04-present)

Companies have so far weathered these challenges well, with U.S. third quarter earnings showing margins expanded to 12.3% versus 12.2% in the first half of 2021. Management teams were able to pass on cost increases to customers without any material impact on demand. However, we expect cost pressures are likely to remain a significant headwind in 2022 and only companies with genuine pricing power will be able to continue to raise prices without impacting volumes.Source: BofA Global Research

At Alphinity Global we hold a number of high-quality ‘price makers’ that showed impressive pricing power in the third quarter, including Danaher, Microsoft, ASML, Apple, Prologis, Daimler and Nestle. Below we expand on the latter two and why we expect them to continue managing these challenges to drive better than expected earnings going forward.

Daimler AG (DAI GR): A luxury car (price) maker with grand EV ambitions

Daimler is a leading global manufacturer of luxury cars and commercial vehicles through Mercedes Benz (MB) and Daimler Trucks (DT).

MB aims to be a leader in the transition to electric vehicles. From next year there will be battery electric vehicles (BEV’s) across all segments, and from 2025 onwards customers will be able to choose an all-electric alternative for every model they make. In addition, significant investments will be made in BEV technology, across batteries and charging options. MB aims to drive the plug-in hybrid & BEV share up to 50% by 2025 and be all-electric by the end of the decade.

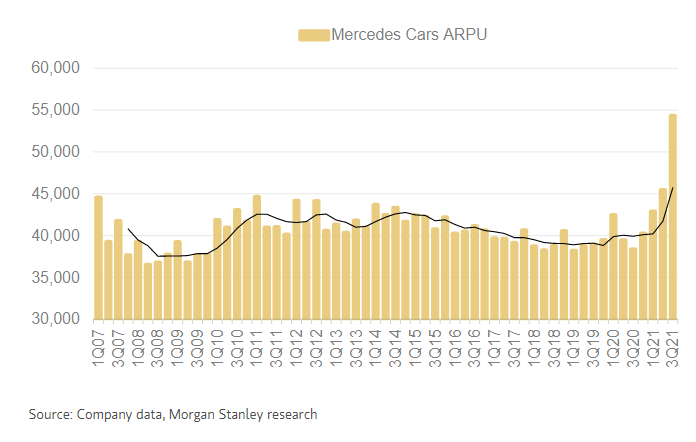

Daimler recently reported strong 3Q21 results, posting flat revenues despite volumes dropping ~30% and significant supply chain headwinds, reflecting the pricing power of their premium brand. The company reiterated margin guidance of 10-12% for cars and 6-8% for trucks despite persistent cost and supply headwinds. The spin off and separate listing of the Daimler Trucks & Buses division was confirmed for 10 December 2021.

Looking ahead, DAI’s “goal is to continue to increase net revenue per unit during the decade, sustainably and significantly”. We expect superior margins performance from positive price/mix and lower costs (a >20% fixed cost reduction by 2025 vs 2019). Adding more high-end, higher margin electric vehicles, ramping up digital service revenues and switching to a direct sales model will also contribute.

Mercedes Cars – Average Revenue per Unit continue to climb

Further, we expect that the spinoff of Daimler Trucks will be a positive catalyst, creating two attractive pure-play entities and unlocking value through a more focused product strategy and better capital allocation. Daimler is currently trading at an undemanding price/earnings valuation of 7x PE, which doesn’t capture the quality of the business and the positive outlook for earnings.

Nestle (NESN SW) – A blue chip defensive with underappreciated earnings growth

Nestle is the world’s largest food and beverage group with operations in more than 70 countries and a broad selection of industry leading global brands including Kit Kat, Maggi, Gerber, Milo, San Pellegrino, Nesquik, Smarties, Aero, Crunchie, Nescafe, Nespresso, and Haagen-Dazs.

Nestle recently reported another quarter of outperformance, reflecting broad-based market share gains across most channels and markets. The high quality 3Q21 revenue beat (+6.6% y/y vs 3.6% y/y expected) reflected both ‘real internal growth’ (volume/mix) and pricing ahead of analyst forecasts. Management also raised their 2021 organic growth guidance to 6-7% (vs previous 5-6%) and reiterated full year margin guidance of 17.5% despite cost inflation and one-off integration costs. Management remain confident that pricing power can offset cost pressures and continue to expect moderate margin improvement beyond 2021.

Starting in 2017 under the leadership of CEO Mark Schneider, Nestle has sold lower growth/margin businesses and recycled the capital to build scale in existing higher growth segments such as coffee, pet care and health science. At the same time, management are driving an exciting digital transformation, which aims to accelerate e-commerce as a percentage of sales from 13% today to 25% by 2025, and increase digital marketing spend from 47% to 70% of total marketing spend over the same period. Together we expect that these changes will drive a sustained acceleration in revenue growth, with continued upside in margins over time.

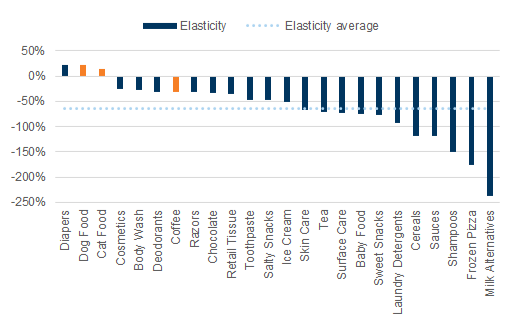

Nestle’s category price elasticity highlights the pricing ability of Nestle in an inflationary environment and points to the attractiveness of its key categories.

Source: Goldman Sachs, 3Q21

Nestle has leading brands in strong categories which offer unique growth and pricing power in a sector which is likely to struggle to cope with rising costs and the continued threat of private label brands. The chart above illustrates the strength of pet care and coffee, two categories where Nestle enjoys leading market positions. The forward PE is ~25x, with a growing dividend yield of ~2.4% p.a. Nestle is a high-quality defensive business with under-appreciated earnings growth – perfectly positioned as a safe-haven in an environment which remains fluid and uncertain.

Author: Elfreda Jonker, Client Portfolio Manager

This material has been prepared by Alphinity Investment Management Pty Limited (ABN 12 140 833 709 AFSL 356895) (Alphinity). It is general information only and is not intended to provide you with financial advice or take into account your objectives, financial situation or needs. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. Any projections are based on assumptions which we believe are reasonable but are subject to change and should not be relied upon. Past performance is not a reliable indicator of future performance. Neither any particular rate of return nor capital invested are guaranteed.