That’s not a peak……

I still remember the time I thought I’d hit “peak technology”. I had a new Nokia 3310 in my hand and after making a call and sending an SMS I found a game called Snake that helped to pass time in the cab while the driver fumbled through a UBD street directory to try and find my hotel. I was also carrying a new digital camera to document my trip and an MP3 player with music I’d burned from my existing CD’s. And when I hit my destination all I needed to find was a telephone port to be able to connect back to the work files I needed to finish a presentation for the morning. What a time to be alive….…

It would have been impossible at that time for me to envisage what life would look like 20 years later. The phone I use is now a phone, internet, camera, music and TV device all in one, with the capability to run my entire life off a 6 inch by 3 inch screen. That cab I was in? Well now the guidance systems mean never pulling into a McDonalds to work out directions ever again, let alone the incredible advances in safety features and entertainment. Then we stand at the front edge of the electric vehicle migration while peering at autonomous driving looming on the horizon. Those files I need? Well now I can access them from anywhere and on any device as data migrates to the cloud. The changes to the way we live, and work have been astonishing and are accelerating.

While it is almost impossible to imagine what the next 20 years may look like, one thing we do know is that as technology marches ever forward, so does the required intensity of computing power. It is quite a leap from having a “snake” made of clunky pixels moving on a basic screen to cars that need to observe and assess all factors around them then calculate and execute the best course of action in fractions of a second. Let alone what other currently unimaginable technology extensions will emerge.

Imagination and semiconductors – driving technological advancement

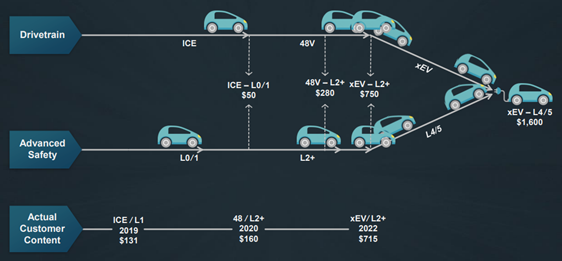

Underpinning this march in computational advancement have been semiconductors. It is advances in semiconductor technology that facilitates this rapid escalation in compute power while also keeping a restraint on device size. And it isn’t just the complexity of the compute but the expansion in use cases that underpins the importance of semiconductors in the technology supply chain. Taking auto as an example, not only are the semis more advanced, but they have proliferated into almost every element of the car, from power to entertainment to guidance systems. The semiconductor company ONSemi estimate the content value of semis has lifted from $50 for an internal combustion engine with no advanced driver assist systems, to a future state of $1,600 for an electric vehicle approaching full autonomy.

Source: ONSemi Investor Day (Aug 21)

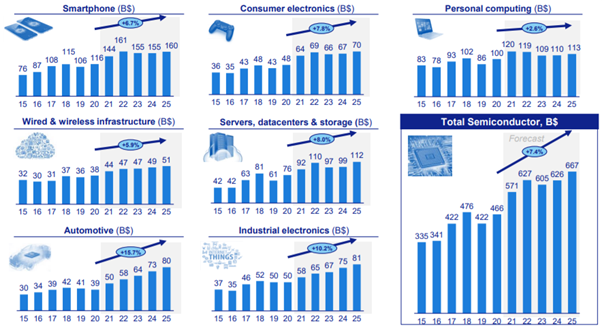

This expansion of content value is occurring across a range of industries. From cars to phones to datacentres and our homes, content per unit is expected to lift by 50-100% when moving from 2020 to 2025. Smartphones are continually adding more functionality, datacentres are adding capacity to underpin advances such as AI, machine learning and the metaverse while compressing speed, and our homes are moving towards a degree of connectivity for almost every device.

Source: UBS (Jan 22), Applied Materials (April 2021)

What does this mean for the semiconductor industry?

This acceleration of technological development has driven a step change in semiconductor industry growth rates, with demand rising from a historical growth rate of 3-5% p.a. to an industry forecast to grow at 6-8% p.a. out to 2030, taking total industry revenue beyond $1bn. Where demand used to rise and fall with smartphone and PC demand, there are now much broader demand drivers, with particular areas of strength expected across autos, industrials and datacentres.

Source: ASML Investor Day (Sept 21), Gartner

How do we invest in this opportunity?

There are many ways to invest along the chain in semiconductors. From the equipment manufacturers (ASML, Lam Research, Applied Materials, ASMI) to the main manufacturers (TSMC, Samsung, Global Foundries, Intel) to the semiconductor companies exposed to different elements of end demand spanning data centre (Nvidia, AMD, Marvell), auto (ONsemi, IFX, Texas Instruments) and memory (Micron, Samsung, Hynix) to name just a few. Each discrete exposure brings with it a nuance to overall semiconductor cyclicality and underlying demand strength.

Our goal is to balance end market demand strength, company positions and financial return metrics with a degree of resilience in the face of an ever present (and sometime violent) semiconductor cycle. Among the swathe of opportunities, our preference currently lies with:

- ASML (equipment manufacturer): the market leader in lithography driving semis manufacturing to ever smaller parameters. The drive for semiconductor supply chains to be brought back to home countries such as the US and Europe is underpinning a wave of equipment investment that will last towards the end of the decade.

- ONSemi (autos and industrial semi manufacturer): ONSemi has reshaped their business towards the key automotive and industrial semiconductor markets, while focusing on value added products within these segments to drive margin improvement.

- Nvidia (GPU and CPU manufacturer): Nvidia is a leader in graphics processing units for gamers which are also being used as datacentre accelerators. Nvidia is also creating semiconductor platforms overlayed with software to drive further opportunities across autonomous driving and the metaverse.

Life in 2040?

The changes to tech have been stunning in the past 20 years and it is difficult to imagine what the next 20 years will bring. But one thing we do know is that compute will advance, and semiconductors will be the key linchpin in assisting this drive forward. As such the future looks bright and the return profile compelling for those that can carve out a market position exposed to these key tech growth trends.

Author: Trent Masters, Global Portfolio Manager