The outlook for commodities

Whilst it appears the recent commodity rally is a response to a combination of factors ranging from a weaker US Dollar and improving global demand growth, I believe China remains the dominant driver of higher commodity prices. Demand from China has surged since the end of 2015 on the back of stimulus injection via its infrastructure and property engines. In parallel, its aggressive pursuit of capacity and environmental reform is strongly affecting the supply dynamics of commodities such as iron ore, coal, steel, aluminium and copper. Speculators have jumped on that thematic and are pushing prices, in some cases to levels above what fundamentals would suggest.

Whilst the rally is not sustainable longer term, the upcoming government transition in China and winter closures is likely to provide ongoing support over the next 6 months. Eventually prices will correct on any sign of demand weakness and/or policy relaxation. It is inevitable given China cannot keep growing its infrastructure and property sectors at the current pace.

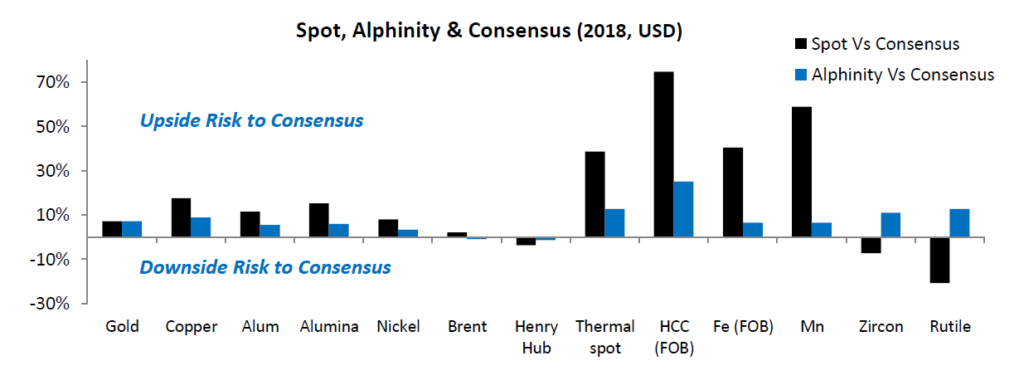

We believe however that market expectations for commodity prices remain too far below the level of current spot prices. As expectations adjust, there will be momentum for future commodity price upgrades, further supporting earnings and share prices. A snapshot of spot prices vs market expectations and Alphinity expectations displays strong upside for CY18, providing a supportive tailwind.

Rio Tinto remains an attractive investment

Rio Tinto (ASX:RIO) offers for us the best upside from both an earnings and valuation perspective. The business is primarily exposed to iron ore, copper and aluminium via their tier 1 long life, low cost assets. Should current spot prices hold, earnings will be almost double what the market is expecting in CY18. Whilst we are expecting a commodity price normalisation, we still believe the market appears overly cautious. For example Copper price expectations are 2.5$/lb for CY18 vs a spot price above 3.0$/lb. The lagged demand impact from China infrastructure, property fit out and grid tendering combined with a likely ban on China scrap imports will keep the market tight. The dynamics for Aluminium with policies putting a cap on supply growth combined with cost increases are also compelling implying a higher floor than the one expected by the market.

In addition to RIO’s broad portfolio exposure, we also like management’s approach to active divestment of non-core assets, its large brownfield investments and its well capitalised balance sheet. This provides the business optionality to pursue capital management initiatives and attractive opportunities as they arise. Flexibility combined with discipline is a potent combination.

Portfolio positioning

The overweight position to the Resource sector over the majority of CY 2017 has been an important contributor to the outperformance of the Alphinity strategies over the last 12 months. Lifting commodity prices combined with operational efficiency improvements and low capital expenditures has allowed miners to substantially improve their balance sheets whilst at the same time deliver appealing capital management programs.

We remain positively disposed to the sector through selective commodity and company specific exposure as we believe these dynamics continue to remain underestimated. Key overweight positions include RIO (discussed above), S32, BSL, SGM, OZL and NCM. All investments display intrinsic compelling investment drivers over and beyond commodity price upside.

Want more information?

Author: Stephane Andre, Portfolio Manager