Who: Shane Kelly

Where: USA

When: March 2016

What were you looking for?

In March I spent a week traveling throughout the US in order to gauge the rate of recovery taking place in the US homebuilding sector which was significantly impacted by the Global Financial Crisis.

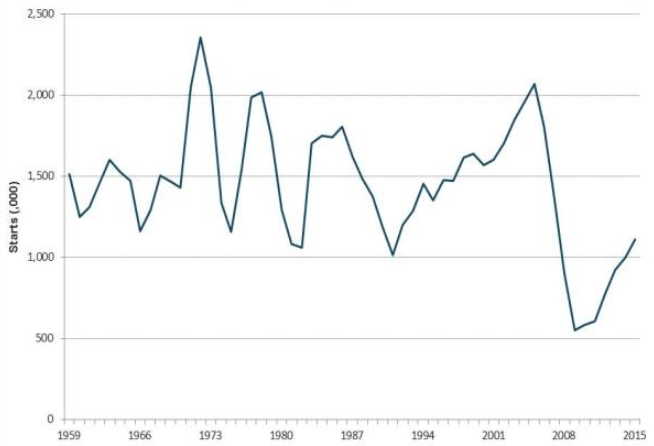

We are 7 years past the peak of the crisis and from a financial markets perspective, many equity markets have returned to or have exceeded previous highs. The only laggard is the US housing sector; it still has some way to go before reaching previous cyclical norms, let alone cyclical highs. In the 50 years prior to the GFC the US housing market on average built 1.5 million new homes a year and no less than 1.0 million new homes a year. This dropped to a new low with only 550,000 homes built in 2009.

Over time, the housing sector began to show signs of recovery and so did the general US economy. More and more new homes were built in both 2012 and 2013 which lead many economists and analysts to forecast a continued linear recovery. This however proved too optimistic and over the past two years the rate of recovery has been more modest than initially expected.

From an investment perspective, these high initial forecasts and the subsequent negative revisions flowed directly to forecasted earnings of building related companies. This has led to earnings downgrades of such companies, irrespective of operational performance.

The slower than expected recovery has been attributed to a range of factors, including access to credit as banks tightened lending standards, younger people choosing either to stay at home longer or rent rather than purchase a new home, housing affordability and labour constraints. All of the above have acted to restrict the number of new homes that can be built.

Chart 1: US Housing Starts

Source: Bloomberg, Alphinity

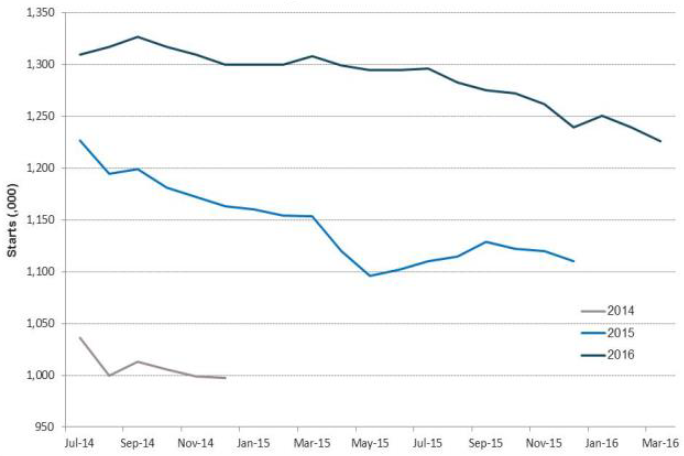

Chart 2: US New Housing Starts – Consensus Forecasts

Source: Bloomberg, Alphinity

What did you discover?

Current consensus forecasts are for 1.2 million new homes to be built during 2016, which is a 10% increase on the 1.1 million built in 2015 and consistent with the growth rate experienced over the last year. Based on the meetings I had, these forecasts seem reasonable in what I would describe as a solid environment for new home construction.

The key factors behind this conclusion are:

- Interest rates and credit availability: Currently the interest rate on a 30 year fixed rate mortgage in the US is just above 4.0%, more than 30% below the average rate in the 10 years prior to the GFC. This reduced interest burden coupled with a gradual easing in credit conditions is allowing more Americans to secure mortgage financing.

- Household formations: Given the severity of the last recession, many people were forced to either move back home with their parents or delay moving out of home. Driven by a strong recovery in the job market over the last few years, household formation rates are now beginning to rise above historical averages. As new households form, vacancy rates on existing homes drop and rents rise. In response, more people look to buy new homes. Millennials (Gen-Y) are also buying their first home (age 31-35) which should further support house formation over the next few years.

- Household affordability: Offsetting some of the positive demand factors highlighted above is a limited supply of affordable housing stock. Increased consumer costs especially in health care, large student loans and strong house price growth were all factors highlighted as holding back demand, especially amongst first time buyers. Some builders have recognised this and are now starting to focus on providing more affordable entry level homes.

- Labour supply: A consistent theme amongst the home builders I met with was a shortage of labour, particularly in specialist trades. The construction sector in the US has for many years relied on migrant workers many of whom left the US during the recession and who can no longer re-enter. A large number of specialist tradespeople also left the industry and whilst some may return, especially those that moved across to the energy sector, the current shortage will hold back the growth rates achievable in new house construction, irrespective of demand.

What does this mean for the Alphinity portfolio?

With more moderate increases in housing start growth predicted over the next year we feel more confident that earnings expectations for building materials stocks are also more achievable. At present the portfolio has an overweight position in James Hardie that we expect will benefit from both the pick-up in underlying housing growth as well as its fibre cement product continuing to take market share from alternative materials.