Who: Jeff Thomson, Portfolio Manager

Where: Sweden/Denmark

When: March 2017

Nordic financials tour

Where did you go?

I recently toured Stockholm and Copenhagen visiting senior management from all the major regional banks, including a meeting with the Swedish FSA. I also met with two of the biggest P&C insurers in the region (IF & Trygvesta), as well as the CEO of the largest Nordic payments company (Nets A/S).

What were you looking for?

Insights into the outlook for Nordic financials generally, but also specifically for Danske Bank where we currently have a position.

What did you discover?

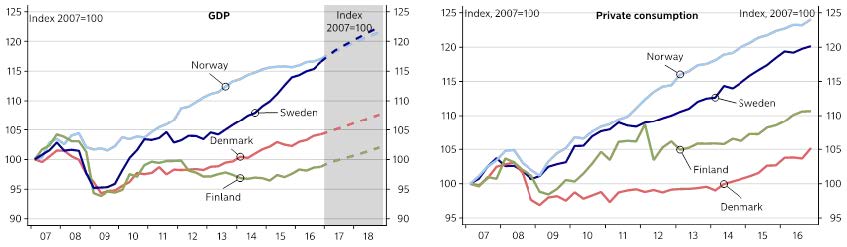

The Nordic economies are generally doing well, led by Sweden.

The Nordic region appears to be doing well, with Sweden especially strong recently led by personal consumption. There was some talk about the start of a new corporate capex cycle in Sweden, with industrial capacity utilisation apparently close to 100%.; However consensus views were mixed on the subject with just as many cautious on calling this.

Denmark is also beginning to grow again, although at a slower pace than Sweden; following a more severe housing correction in 2007/8, it seems that Denmark is several years behind Sweden in the recovery cycle. Despite the recovery in oil prices, parts of Norway are still struggling with issues associated with the recent collapse in the oil price – mainly in oil services supporting offshore drilling.

Chart 1: The Nordic economies are all expanding, with Sweden especially strong

Source: Nordea Markets and Macrobond

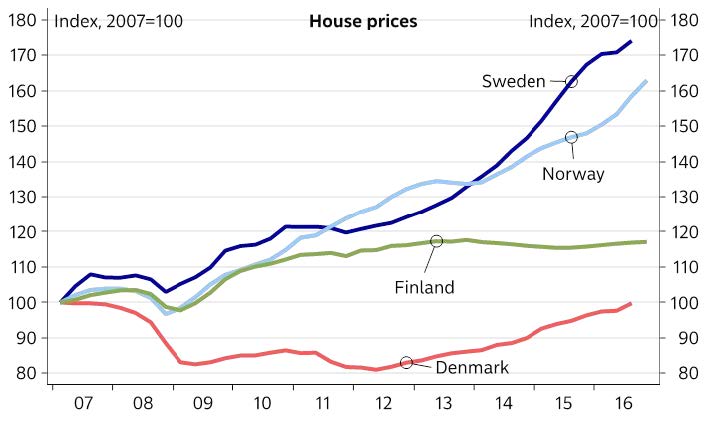

Australia is not the only country with a housing problem

In the words of one US fund manager on the trip: an overheated Nordic property sector poses a “non-trivial risk of a total train smash”. This was unquestionably the biggest theme of the tour, with every meeting discussing the property market in one form or another. There was a general consensus that the situation (especially in Sweden) was serious and posed potentially significant systemic risks for the broader economy; however given strong employment and low interest rates the probability of a severe correction in the short term is low.

Chart 2: Nordic house price growth

Source: Nordea Markets and Macrobond

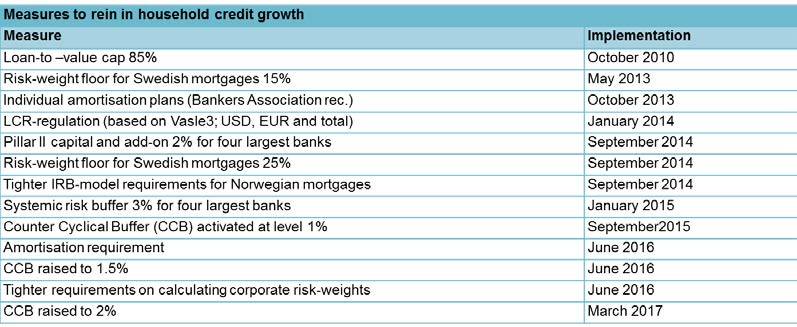

Macro-prudential measures have had a limited impact so far

While it was reassuring to find that all stakeholders in Sweden are focused on addressing property risks, initiatives to date appear to have had a limited impact. Regulators have released a series of macro-prudential measures and banks have all tightened mortgage underwriting standards – stress testing new borrowing at 8%, introducing a leverage ceiling of 5x and actively encouraging fixing rates (with limited success). These measures initially succeeded in slowing house prices, however it appears that prices have recently begun to accelerate again and the regulator is now considering further action including a 600% loan to net disposable income ceiling and possibly mandating fixed term lending for higher risk borrowers. There is also periodic public debate about removing the tax deductibility of mortgage interest, but like Australia this is a political hot potato and seems unlikely to happen.

Table 1: Swedish macro-prudential measures introduced so far

Source: Danske Bank

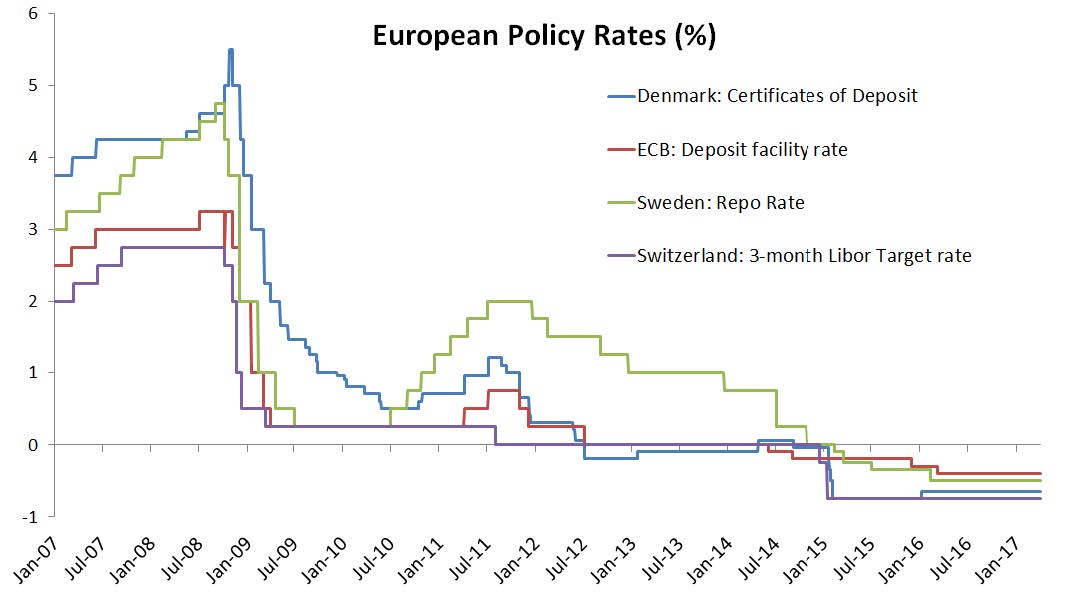

Odds of a Swedish rate rise have modestly increased

Sweden, like most of the rest of Europe, has had negative interest rates for several years. This has been a significant headwind for spread based revenues, however banks have generally adapted well – passing on negative rates to corporate and wholesale deposit holders, but protecting retail consumers. A rational oligopoly has also meant that the banks have successfully re-priced lending to reflect low/negative deposit margins as well as higher regulatory capital requirements. On the corporate side, explicit interest rate floors have been introduced. High loan-to-deposit ratios have also helped.

Chart 3: Negative Policy Rates in Europe

Source: Bloomberg & Alphinity

Rate increases by the US Federal Reserve and improved growth mean that there is now a small but growing prospect of modest rate rises over the next 12-24 months in Sweden (and possibly Europe). In the very short run Nordic banks are unlikely to enjoy the same sensitivity to rising rates as Italian and Spanish banks; for the same reasons that they have been relatively resilient under negative rates (i.e. corporate rate floors and high loan-to-deposit ratios). Nevertheless, over time gradually higher interest rates would be a material positive for spreads, albeit potentially offset by slower growth and higher property related credit risks.

Capital adequacy remains a hot topic

Nordic banks have superficially high capital ratios; however this largely reflects low underlying mortgage risk weights (e.g. ~7% in Sweden given very low historic loss experience) and increasingly cautious pillar 2 regulatory overlays and management buffers to compensate for this. Over and above the clear systemic risk posed by elevated property prices, there remains a high probability of some form of risk weight inflation from pending regulatory reform (so-called ‘Basel IV’). At its worst (output floors of 80-90%) the sector could still face a significant potential capital shortfall; although a more benign (and more likely) outcome could see capital returns accelerate as the increased certainty allows regulators and management to reduce buffers.

Nordic banks

Nordic banks are generally viewed as either well worth the premium, or alternatively too expensive given the risks. My conclusion following the trip is that these are mostly strong franchises, which are well managed, thoughtfully regulated and, in Sweden, operate within a rational and shareholder-friendly oligopoly. Both Nordea and Svenska Handelsbanken are potentially interesting investments although better entry points are likely to emerge as some of these property risks play out. The trip also largely confirmed my conviction around Danske Bank, which is likely to surprise on loan volume growth and is underwritten by an almost double digit total yield; there is additional optionality from an improving Danish economy and further mortgage re-pricing.

What does this mean for the Alphinity portfolio?

The investment trip was encouraging as it confirmed that underlying growth in Europe appears to be improving and the prospect of rising rates – a positive catalyst for the sector – has increased, albeit only very modestly. Of course the path to normalization in Europe remains far from clear and at a minimum it seems certain to involve periodic episodes of significant volatility. There are several important political elections over the next 12 months which pose clear tail risks to the outlook. As a consequence our investments in the region are selective and, as always, focused on attractively valued, high quality franchises where we have visibility on earnings upgrades.