Who: Jeff Thomson, Portfolio Manager, Alphinity Global Equity Fund – Active ETF

Where: Boca Raton, Florida

When: February 2019

Where did you go?

I travelled to Boca Raton in Florida to attend the CAGNY 2019 conference. The Consumer Analyst Group of New York (CAGNY) is a not-for-profit organisation connecting investors, sell-side analysts and management dedicated to the Consumer industry (mostly Consumer Staples companies). The Conference was attended by c.850 investors and senior management teams (mostly CEO’s and CFO’s) from 31 different publicly-listed consumer companies.

What were you looking for?

I was looking for insights into the outlook for the Consumer Staples sector generally, but also specifically for updates from Mondelez International Inc., currently one of the Alphinity Global Equity Fund – Active ETF top ten portfolio positions.

What did you discover?

The outlook for the Consumer Staples sector remains difficult. Increased awareness of issues around health, wellness and sustainability are rapidly changing consumption preferences, at the same time our modern “on-the-go” lifestyles are multiplying consumption occasions. Distribution channels are also shifting, reducing barriers to entry for newer ‘on-trend’ brands, while private label continues to pressure pricing for weaker and less innovative products.

It’s no surprise that this is presenting significant challenges to the larger incumbent Consumer Packaged Goods (CPG) companies. Management generally has strategies in place to address these issues but, despite some early signs of improved top-line momentum, earnings currently remain under pressure from reinvestment initiatives, inflationary cost pressures and FX. There are several macro themes worth highlighting:

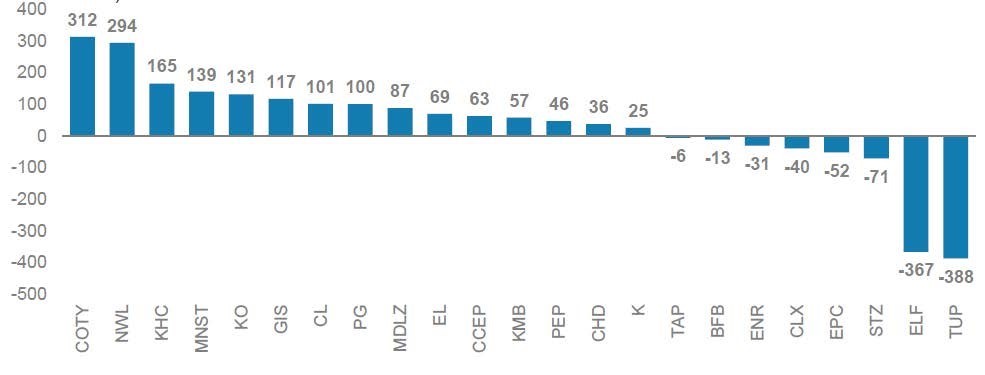

Pivot away from margin expansion to top-line growth: Almost without exception, all CPG companies are now re-focused on accelerating revenue growth. After several years of targeting margin expansion with aggressive cost cutting and efficiency measures, there is now universal appreciation that this strategy is ultimately unsustainable without significant reinvestment to support higher and more consistent revenue growth. A point sharply underlined during the week by the dramatic profit warning from Kraft Heinz, the 3G-led poster child for aggressive ‘Zero-Based Budgeting’ – a timely reminder of what can happen when margin expansion opportunities are exhausted and the ‘growth-music’ stops. The focus has shifted away from ambitious margin targets, which potentially constrain growth, towards maximizing margin dollars which can be reinvested back into revenue growth, starting a virtuous ‘profit fly-wheel’. There are some early signs that sector revenues are accelerating (see chart 1), although there are still valid questions around the cost and sustainability of this recovery.

Chart 1: Top-Line Growth is Improving

Last Quarter 2-Yr Avg Organic Sales Growth vs. Last 12 Months (bps difference)

Source: Company data, Morgan Stanley

Cost of growth: It’s proving difficult and expensive to reverse a multi-year trend of low and even negative sales growth given the competitive sector dynamics. A large part of the new growth algorithm involves pushing into new adjacencies, segments, geographies and distribution channels – to ensure that opportunities are captured across all consumption occasions and sales channels. This generally means an increased focus on smaller, more local brands, which have been neglected over the last several years.

Product innovation was also a strong theme throughout the week, with increased investment behind initiatives to improve the impact of innovation through improved execution. For example, Mondelez talked about focusing on ‘speed over perfection’, and ‘agility over process’.

All of this clearly comes at a cost and can be margin dilutive before/until revenue growth can manifest itself.

The jury is still out on how successful these initiatives will be and there is a risk that revenue growth remains elusive and/or the cost of growth is structurally higher (i.e. lower margins).

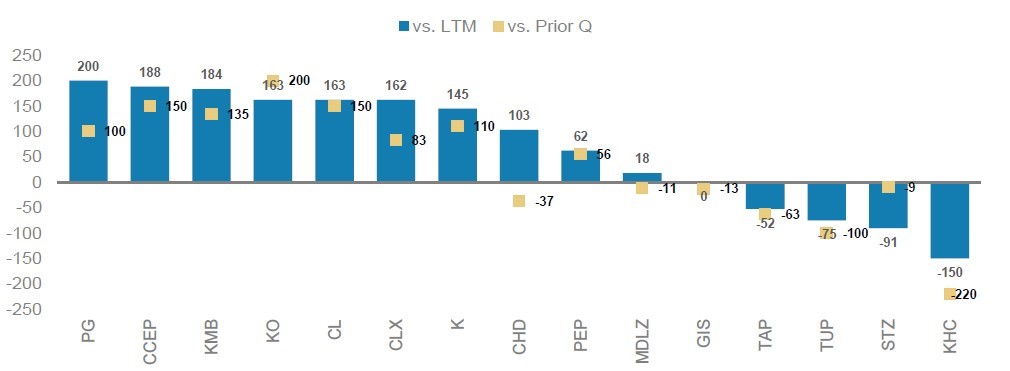

Pricing: This was another prominent theme, with most companies talking about having taken price over the last few months on at least a part of their North American portfolios to compensate for higher commodity, transport and labor costs. Pricing appears to have been well-received so far, however open questions remain around volume elasticities and competitive responses. If these increases stick this could boost gross margins in the latter part of this year. It’s also encouraging that oil and resin prices have both weakened recently. Price/mix is also been targeted through product innovation, including pack architecture.

Chart 2: Price/Mix Has Inflected Higher

Last Quarter YOY Price/Mix Growth vs LTM/Q4 (bps)

Source: Company data, Morgan Stanley

FX: Currency translation is still an earnings headwind for most U.S. multi-nationals, with several key currencies (e.g. Euro, Turkish Lira, Indian Rupee, Australian Dollar, Chinese Yuan) weaker y/y, although at current rates this will dissipate as the year progresses.

Areas of growth: Several companies (e.g. Mondelez & Kellogg) talked positively about emerging markets, where demographics and a growing middle class are tailwinds. Other focus categories included pet food, coffee, snacking, and high-end cosmetics (L’Oreal). In contrast segments like breakfast cereal remain structurally challenged.

Health & wellness: The shift towards healthier, more natural and better-for-you products was widely evident within product innovations. Pepsico continues to drive reduced salt, fat and sugar; Mondelez plans to launch a 30% reduced sugar version of Cadbury Dairy Milk and Colgate is rolling out a new ‘Naturals’ range of toothpastes.

Sustainability: A strong theme with initiatives around responsibly-sourced ingredients, reduced plastics/ packaging/waste and giving back to employees/communities. For example, Coca-Cola European Bottlers target at least 50% recycled PET (vs 28% currently) and 100% recyclability (vs 98%) and collection (vs 74%), by 2025.

Divestitures: Recently large sector deals including Campbell Soup/ Snyders-Lance, General Mills/Blue Buffalo, JM Smucker/Ainsworth and Conagra/Pinnacle have not been well-received. Part of this is due to relatively high valuations, but caution around leverage has also been a factor. Consequently, the tone around larger deals were noticeably more cautious. Strategic bolt-on deals remain on the agenda, but several companies (e.g. Constellation Brands, Kellogg’s, General Mills) talked about divestitures of non-core assets to improve focus and organic growth.

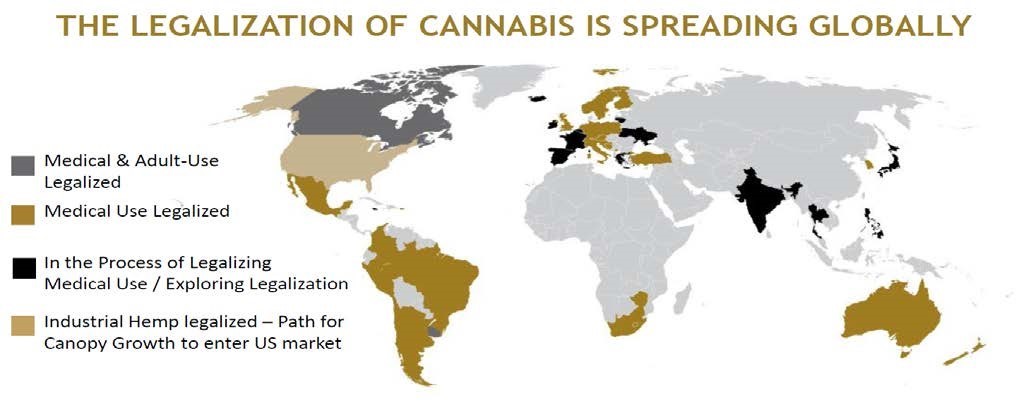

Cannabis: One of the most interesting presentations was from Canopy Growth – a leading cannabis company. Cannabis is likely to be a significant disruptive force across athletic drinks, animal health, anxiety, PTSD, pain relief, sleep, health & wellness and beverage alcohol. Canopy conservatively estimates the global opportunity to be >$500bn. The company is also building IP leadership in the category with 15 human and four animal trials currently underway in Canada around various potential anxiety and sleep indications. Canopy has also registered 32 patents, with another >140 pending, in areas including cannabis-based beverage production, medical treatments, device & delivery technologies, processing and plant genetics.

Source: Canopy Growth

What does this mean for the Alphinity Global portfolio?

Revenue growth will likely be the predominant fundamental differentiating factor over the next few years and it will be businesses in advantaged categories and geographies, and those who are best able to adapt to changes at retail (e-commerce, convenience etc.) and consumer preferences (local, health & wellness, sustainable etc.), that will ultimately be most likely to succeed.

As such I came away with increased conviction around our current investment in Mondelez International Inc. This remains one of the fastest growing US food companies, with organic sales growth well on its way to 3%+ this year. There are structural tailwinds behind snacking and emerging markets (37% of group revenues) which underpin this growth. Mondelez enjoys a no. 1 market position in three of its’ four categories and seems best positioned to successfully execute on a more-balanced top and bottom-line growth algorithm.

Procter & Gamble, Colgate, Pepsico and L’Oreal are all potentially interesting although these stocks currently either lack earnings leadership and/or have elevated valuations, which mean we remain on the side-lines for now.

Author: Jeff Thomson, Portfolio Manager