In the 1980 blockbuster, The Empire Strikes Back, Master Yoda utters the line: “Difficult to see. Always in motion is the future”.

If Master Yoda hadn’t been a Jedi warrior, he would have been a great fund manager. Because even though he was able to partly see the future, he still understood his limitations.

Risk can be so many different things, from the individual stock level all the way up to career risk. The best definition I know is “making decisions when you don’t know the future”.

That captures what risk means to a portfolio. We make decisions today in the portfolio, and when that portfolio meets the future, things happen. Hopefully good things.

Bottom up is better in an uncertain macro environment

The first thing to accept is that there are many factors and risks where we don’t know the exact outcome. We can have views and thoughts, but these will be lower probability decisions. Once we accept what we don’t know, it’s easier to build a futureproof process and portfolio.

The vast landscape of macro and other top-down factors holds a number of potential traps. Most forecasters have been getting bond yield and interest rate expectations wrong for a long time now, with big implications on markets.

Currencies are another high-level asset class which continues to impact markets but are notoriously difficult to get right. Then we have the debate about how and if you can time style investing – the rotations between value and growth investing.

It is always tempting to adopt a top-down view, a macro lens, and then look at all stocks through this lens. It makes the hunt for investments seems easier; it is a mental shortcut.

I’m not saying these factors don’t participate in driving individual stocks. They do. But to produce more consistent investment returns, we think it is the wrong starting point for equity investing.

We believe an investment process is better off being founded in bottom-up fundamentals, and then taking these macro factors into account when analysing different scenarios and risks to these stocks. Even if you can’t predict, you can still prepare.

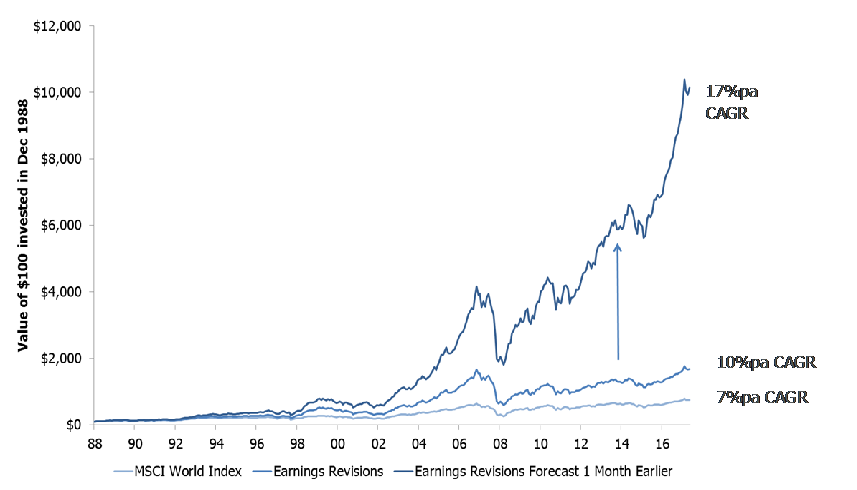

Figure 1 shows that MSCI World, worth $100 in 1988 was sitting at just over $700 at end 2017. That’s a 7 per cent p.a. compound return. Very attractive.

This illustrates lesson 1: you want to invest in global equities long term.

If you instead just simply rank all stocks on earnings revisions over the past three months, and buy the top 20 per cent of the stocks, you turn $100 into almost $2000 (that’s 3 per cent p.a. compound above the market).

Lesson 2 is that earnings revisions drive share prices. If, through good fundamental analysis, you can instead buy this top bucket of upgrading stocks just one month in advance, you would turn $100 into over $10,000 (that’s 10 per cent p.a. compound above the market or 17 per cent p.a. compound.)

Finally, lesson 3: Adding a bit of foresight massively improves the outcome.

The evidence says that a positive earnings announcement by a company is more likely than not to be followed by a period of sustained positive earnings revisions/surprises driving share price outperformance (and vice versa for negative earnings announcements). In short, price momentum and earnings momentum go hand in hand.

This makes intuitive sense, but why does it exist and how do you exploit it?

Observable biases lead to consistent behaviours

In Berkshire Hathaway’s 2014 annual report, legendary investor Warren Buffett said: “In the world of business, bad news often surfaces serially. You see a cockroach in your kitchen, as the days go by, you meet his relatives.”

Buffett was referring here to inherent human biases and flawed corporate behaviours, as well some built-in flaws in our financial markets. For example, company managements try to manage expectations both on the way up and down to maximise their own careers.

And then there are the thousands of sharp analysts out there. Most of them are not incentivised to get earnings right ahead of the curve. They move in herds, to manage their own career risk. They are not primarily paid to get it right. A portfolio manager on the other hand, is incentivised to try and get it right, certainly if working in a sharp boutique environment.

Fundamental analysis, however, is able to foresee earnings upgrades and downgrades. Adding data analytics tools and quantitative analysis gives a higher level of discipline and counteracts your own emotions and biases around that analysis.

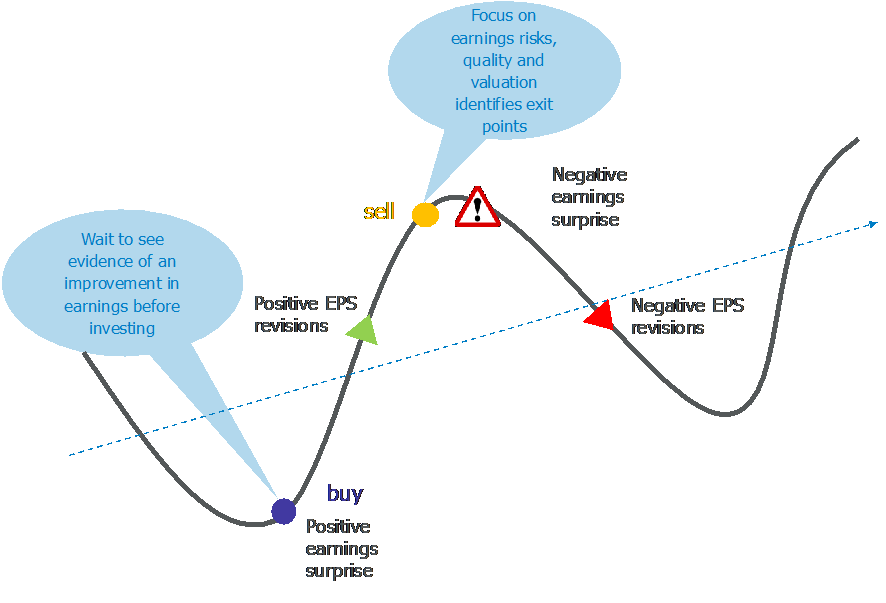

Investing at the right time of the earnings cycle

An Alphinity Investment Management tenet is that earnings can help lead you to the right stocks. There is a consistent opportunity here, as long as you do the analyst legwork on companies and their earnings.

It is about looking for quality companies which are undervalued, but what is clearly differentiated is that you have a strict view of when is a good time to own that stock.

Even high-quality companies go through tough periods and cycles, with downgrades, when investors are better off staying away.

What’s interesting is that when the market underestimates the earnings power of a company, it can take a long time for everyone to catch up with the new reality (see Figure 2). The same goes during a downgrade cycle, it is often equally sticky. The earnings expectations are anchored to the past.

Figure 2: Finding quality, undervalued companies that deliver earnings ahead of expectations

Where is global earnings leadership right now?

The global universe is full of stock picking options, but what types of stocks are currently in the right time of their earnings cycles?

We have been in a broad global earnings downgrade cycle for over a year now. It started in emerging markets, swept via Europe and hit the US at the end of last year.

This is the normal way of things – expectations were just too high again after synchronised global growth plus tax cuts, and analysts have been spending over a year trying to catch up with the weaker reality.

What’s even more interesting are the “internals” of the market, or the relative leadership. Cyclical stocks had a clear leadership in the previous, strong global upgrade cycle of 2016-17, but they gradually lost that leadership from 2018.

The relative earnings leadership continues to sit firmly on the more defensive, quality and growth side. That’s the type of stock which is leading, looking at the big picture. This trend is clear and consistent.

But, let’s pause and think of Master Yoda: “Always in motion is the future”. Just because the leadership is clear now, does not mean it’s time for complacency. Quite the opposite.

The leadership is guaranteed to change, even though we haven’t seen a strong enough trigger for change yet. But it will come, and we should follow it when we get conviction in it.

Building a portfolio focused on sustained earnings leadership

Owning a concentrated portfolio of stocks in the right time of their individual earnings cycles helps us achieve the outcomes we want long term, irrespective of where the market heads.

Earnings leadership is a reliable partner, tuning down market noise and helping us avoid making brave top-down timing calls.

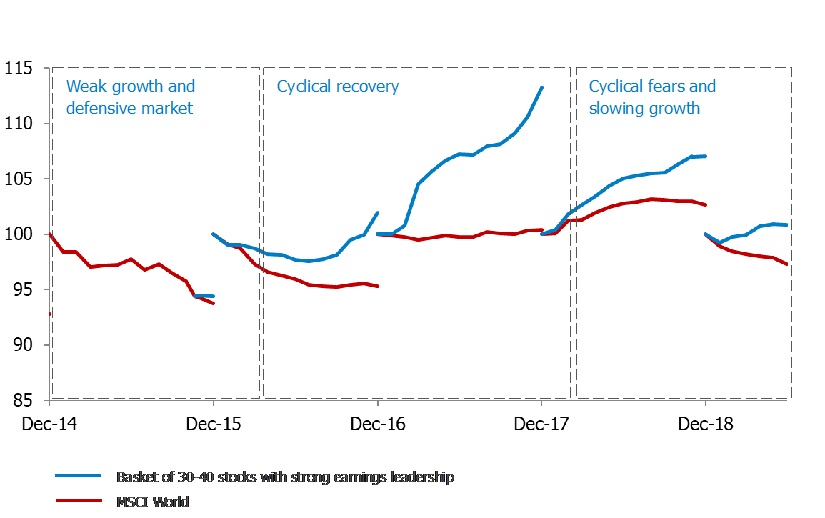

Figure 3 shows how the market’s earnings forecasts (expectations) have developed for the global index, and for a portfolio of earnings leaders.

It has been possible to find stocks with better earnings revisions consistently, even though the market has gone through some material rotations in the past few years.

We have gradually changed the portfolio stocks as a result. Some stocks have lasted through all gyrations, their earnings stories are powerful and idiosyncratic enough, whereas other stocks have had to be replaced.

Not everything has to change but put another way: the portfolio which performed well in 2017 would have had no chance to outperform in 2019. When the facts change you change with them.

This approach is more unconstrained from the macro backdrop and we believe it enhances long-term returns and protects against unintended risks. This agility leads to performance consistency.

Figure 3: Persistently better earnings momentum through different market environments

To state the obvious: Investing is difficult. It’s not supposed to be easy. I personally find the current environment, with its gyrations, extremely challenging.

So, we need an approach that helps us pick risks that we better understand, and helps us make good, informed decisions regardless of where the market takes us.

Investing in stocks with global earnings leadership is one such approach that will help to futureproof a portfolio.

Author: Jonas Palmqvist, Portfolio Manager