With Alphinity celebrating its 10th anniversary we have explored what has happened in the healthcare sector in the decade since Alphinity was first established.

Over this period healthcare was the best performing sector with revenue growth outstripping the broader ASX200 (excluding healthcare and financials) by almost 6 times. This flowed through to far superior earnings growth, which consistent with our investment philosophy, was accompanied by expanding valuations. The combination of stronger earnings growth and higher valuations drove significant healthcare sector outperformance such that healthcare is the now the third largest ASX200 sector.

In addition to strong structural drivers, healthcare sector revenue and earnings growth over the period was supported by a combination of successful R&D programs and offshore expansion. The medical technology and biotech companies have successfully developed new products that both expand the addressable market and capture market share. While some of the healthcare service providers have successfully grown offshore both organically and through acquisition.

We demonstrate this all below in the 10 charts that follow.

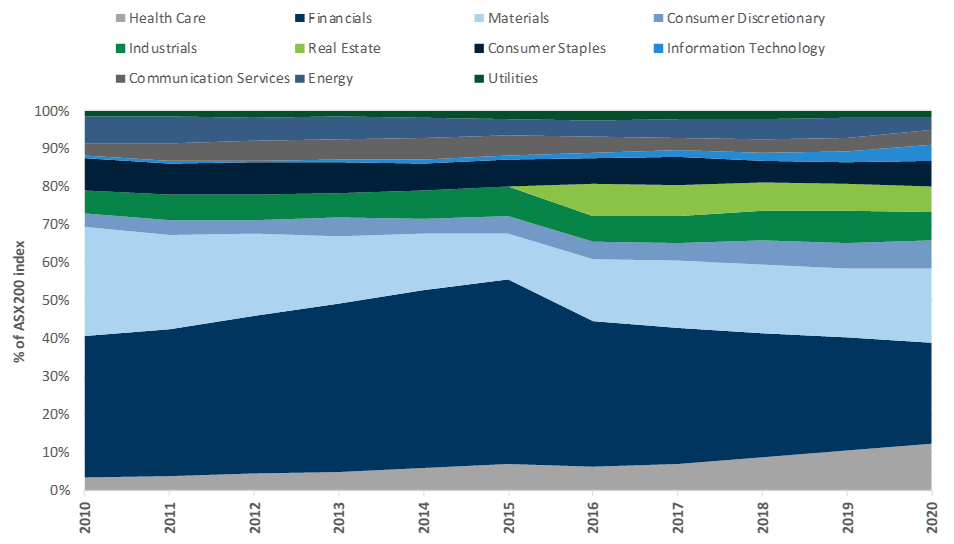

Over the last 10 years the Australian healthcare sector was the best performing sector, growing from 3.3% of the ASX200 index in 2010 to 12.2% today.

Chart 1: ASX 200 sector index weight

Source: Goldman Sachs. As at 28 October 2020.

This outperformance is partly explained by strong underlying fundamental as the healthcare sector generally enjoys strong demand growth for its products and services driven by a growing and aging populations, the increased prevalence of chronic conditions and the availability of innovative new treatments that improve health outcomes.

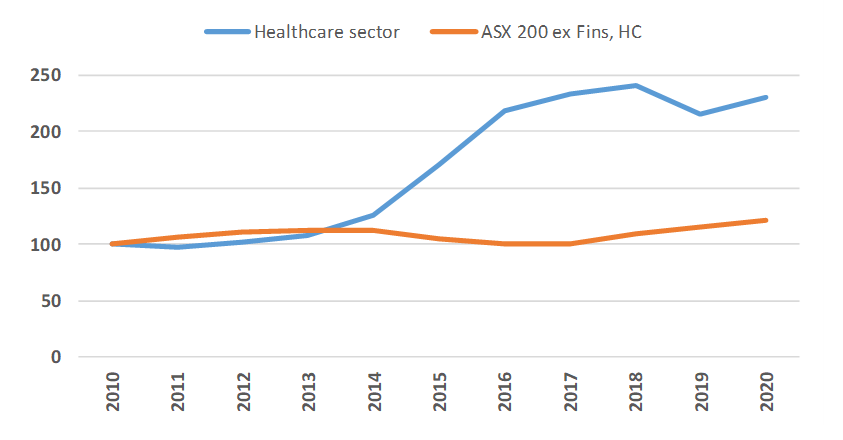

These structural growth drivers have contributed to the healthcare sector growing revenues by 130% over the last decade, well ahead of the ASX200 (excluding healthcare and financials), which only delivered 22% revenue growth over the same period.

Chart 2: Revenue – Healthcare vs ASX200 ex HC & fins

Source: Goldman Sachs, Alphinity. As at 21 September 2020.

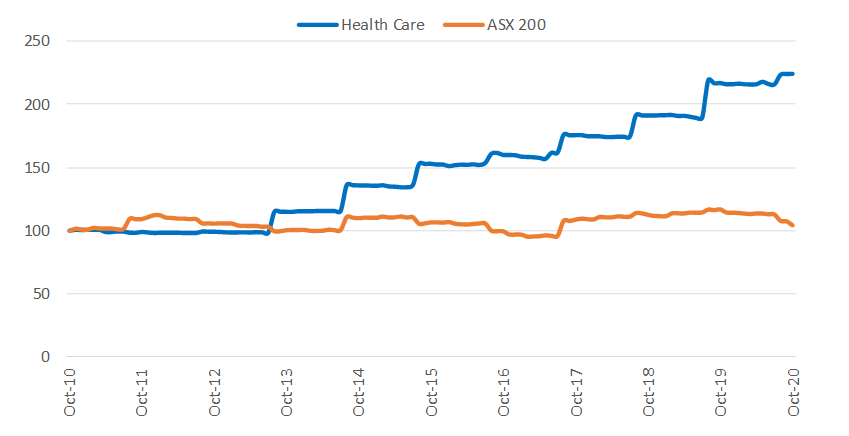

Stronger revenue growth has flowed through to much better earnings growth for the healthcare sector. The healthcare sector more than doubled earnings over the last decade, while the boarder ASX200 only delivered mid-single digit earnings growth, weighed down by the banks and miners.

Chart 3: Earnings – Healthcare vs ASX200 (2010 rebased to 100)

Source: Goldman Sachs, Alphinity. As at 30 October 2020.

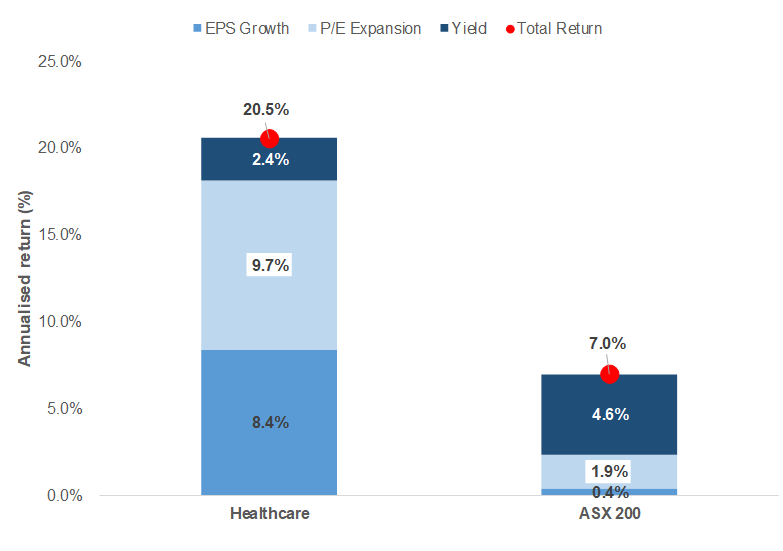

While the healthcare sector has grown revenues and earnings significantly faster than the broader index over the last decade, another reason for the sector’s relative outperformance has been increasing valuations. The market ordinarily rewards faster earnings growth with higher valuations. This has particularly been the case over the last decade as healthcare’s long duration structural growth has been highly sought after in an increasingly uncertain, low-growth world that has ushered in an era of low interest rates.

Chart 4: Drivers of performance past 10 years

Source: Goldman Sachs. As at 30 October 2020.

Over the last decade the healthcare sector has grown earnings at 8.4% p.a. relative to only 0.4% p.a. for the ASX200. Valuation multiple expansion added a further 9.7% p.a. to the healthcare sector’s total return over the period, relative to only 1.9% for the ASX200.

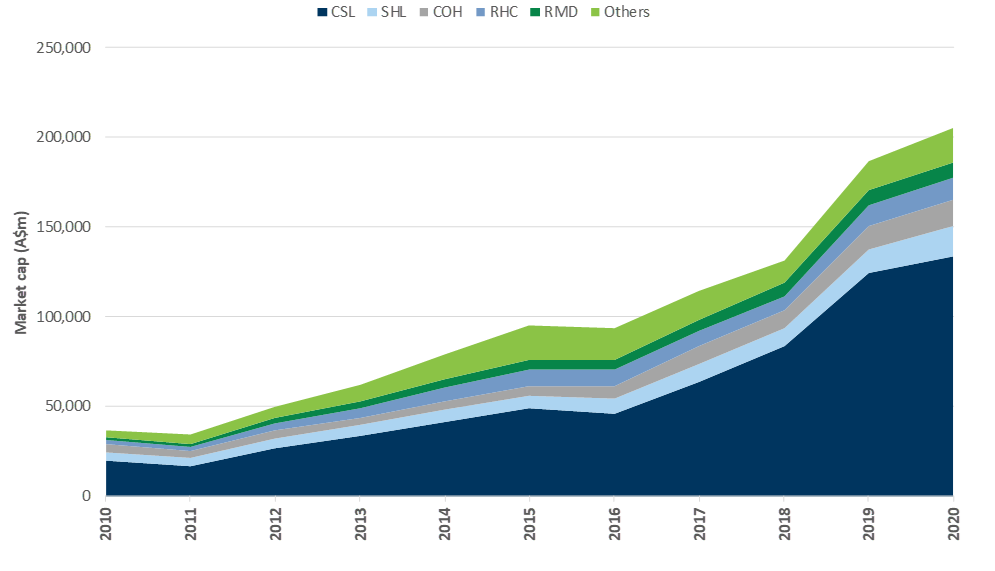

It is always important to consider stock specific factors, particularly given the diverse nature of the Australian healthcare industry. The chart below graphs the healthcare sector’s market capitalisation on a stock-by-stock basis. The most striking observation is that CSL contributed the lion’s share of the sector’s growth over the last 10 years. CSL grew from an index weight of 1.8% in 2010 to 8.0% today, representing approximately 70% of the healthcare sector’s market capitalisation growth over that period. What is even more impressive is that they achieved that without issuing a single share, in fact they bought back stock.

Chart 5: Healthcare sector market capitalisation (A$mn)

Source: Goldman Sachs. As at 28 October 2020.

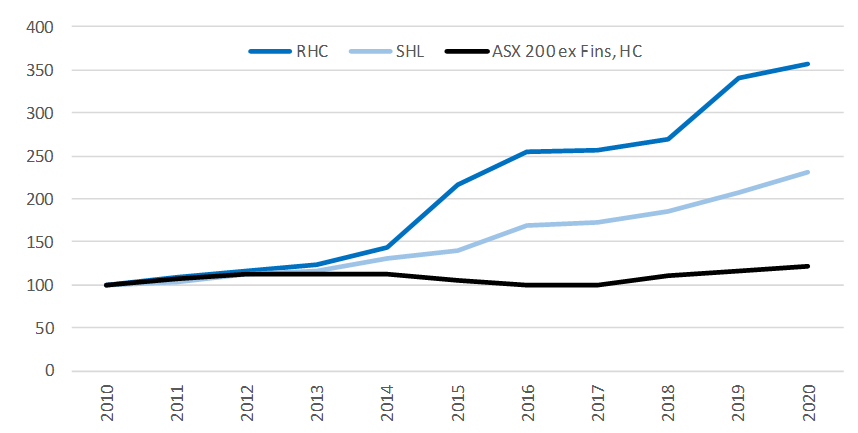

Other stocks such as Cochlear, Ramsay Healthcare, Sonic Healthcare and Resmed have also grown revenues and earnings strongly relative to the broader market and, as a result, have contributed meaningfully to the relative outperformance of the healthcare sector.

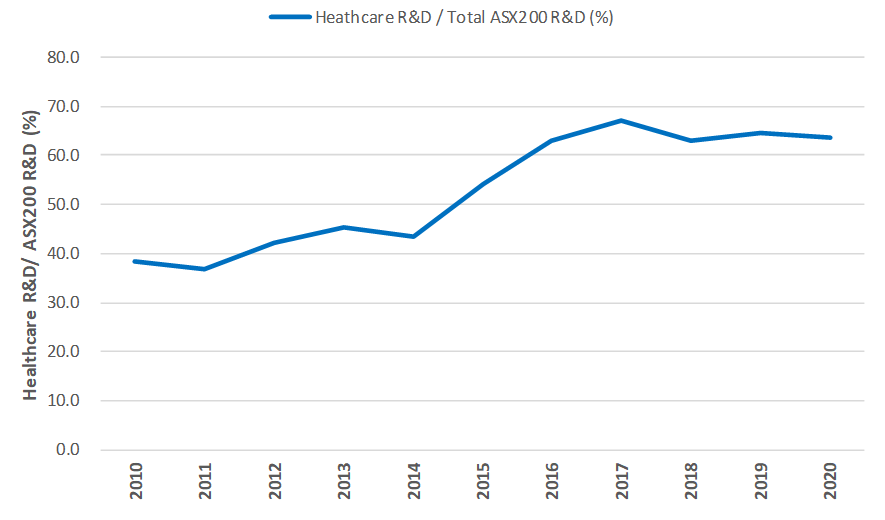

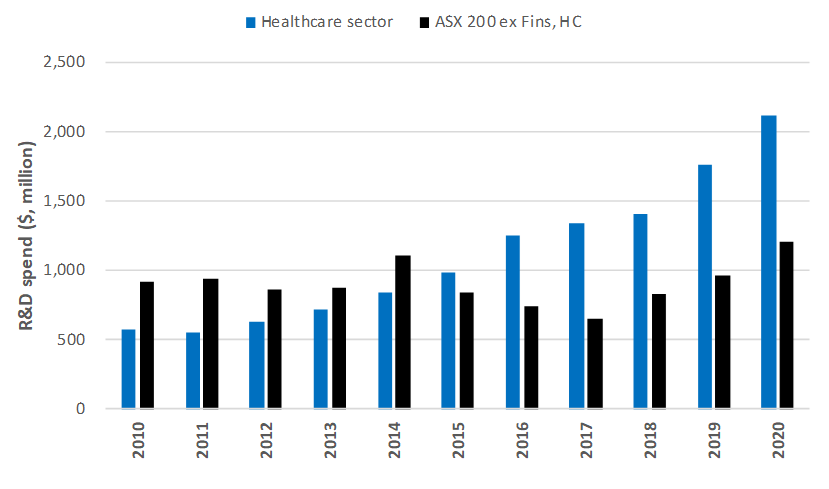

For the medical technology (Fisher & Paykel, Cochlear, Resmed) and biotech (CSL) companies, one source of outperformance has been their heavy investment in R&D, which in many instances has yielded innovative products that both improve healthcare outcomes and grow the addressable market.

The ASX200 healthcare sector has steadily increased its R&D to 5% of sales. Healthcare now accounts for approximately 65% of all ASX200 R&D spending, having doubled its relative share over the past decade.

Chart 6: Healthcare R&D as % of total ASX200 R&D

Source: Goldman Sachs. As at 21 September 2020.

Chart 7: Total R&D spend ($, million)

Source: Goldman Sachs. As at 21 September 2020.

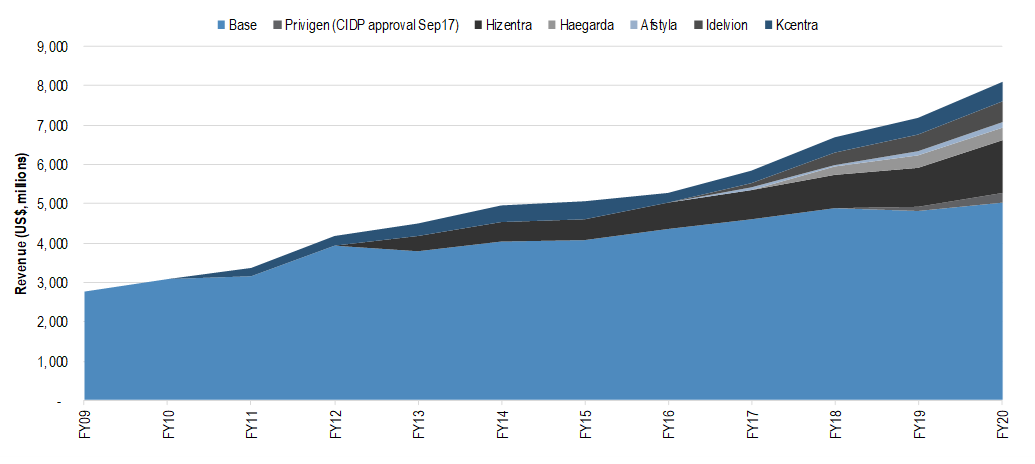

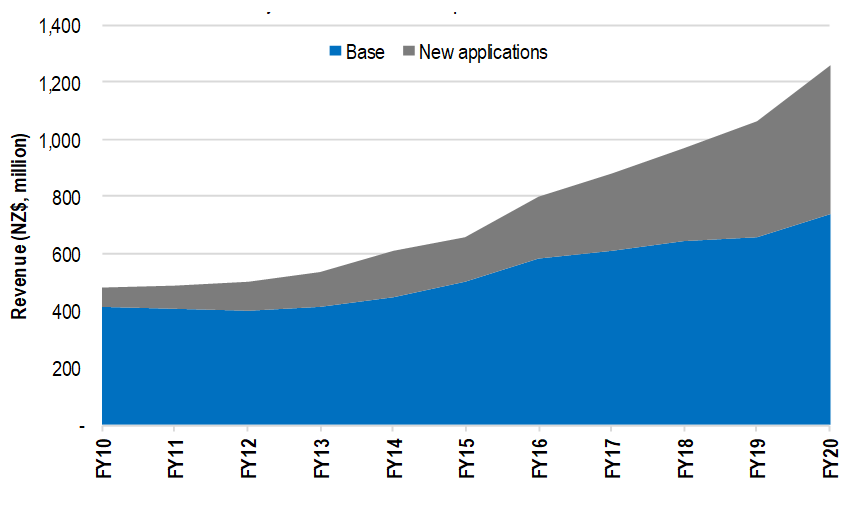

This R&D investment has contributed meaningful growth. For example, the chart below demonstrates the growth CSL has generated, above its base business, through internally generated new products (including label extensions for existing products to new indications). Many of these new products are significantly more efficacious and/or have broader indications, meaning that in many instances they have grown the addressable market while also allowing CSL to take market share.

Just under 40% of CSL’s FY20 revenues were generated by products stemming from internal R&D programs. Given these products are typically very high margin, often being made from leftover source material from the base immunoglobulin business, the earnings contribution from these products would be even larger.

Chart 8: CSL new product revenue contribution

Source: JP Morgan. As at 4 November 2020.

Similarly, Cochlear has lead direct sound streaming innovations in the cochlear implant market and is significantly ahead of any competitors in developing a totally implantable device which has potential to revolutionise the hearing market. Cochlear is also helping accelerate industry growth by developing technologies which expedite the identification of potential cochlear implant patients and which automate treatment processes to free up clinic capacity.

Resmed has continued to invest and develop technologies that improve patient compliance and streamline mask resupply processes, both of which have driven higher volumes for Resmed while also improving economic outcomes for their supply chain.

Fisher & Paykel have developed new respiratory support methods such as high-flow nasal therapy that have been increasingly adopted as the weight of supporting clinical research grows. These efforts have been bolstered recently by COVID. COVID treatment guidelines globally have adopted high-flow nasal therapy as the recommended first-line COVID-19 treatment. FPH’s high-flow nasal canula product (Optiflow) dominates this space. In the short term this significantly increases FPH’s addressable market as almost all hospitalised COVID patients will be treated with FPH products, not just the most severe patients requiring intubation. In the longer term these changes to clinical guidelines are likely to have implication for how all respiratory patients are treated, further expanding the addressable market.

Chart 9: Fisher & Paykel Healthcare new product revenue contribution

Source: JP Morgan. As at 4 November 2020.

New applications, including Optiflow, represented 41% of Fisher & Paykels FY20 revenue and are expected to contribute the majority of growth going forward.

R&D is clearly much less relevant for the healthcare services businesses such as Ramsay Healthcare and Sonic. However, it is worth noting that both these businesses have also been very successful at expanding both domestically and abroad, which has delivered materially stronger revenue and earnings growth relative to the ASX200. Ramsay Healthcare and Sonic have grown revenue +258% and +131% respectively over the last decade, relative to the ASX200 (ex healthcare and financials) only delivering +22% revenue growth.

Chart 10: Revenue – Ramsay & Sonic vs ASX200 ex Fins & HC (2010 re based to 100)

Source: Goldman Sachs, Alphinity. As at 21 September 2020.

In addition to many of the structural drivers previous mentioned, domestic expansion for these companies has also been supported by strong management execution and favourable industry structures. For example, Ramsay Healthcare has benefitted from above system growth and favourable pricing given their large market share and desirable hospital locations. Likewise, Sonic has enjoyed significant scale synergies from organic and M&A driven growth.

While much of Ramsay Healthcare and Sonic’s offshore expansion has been driven by acquisitions, both Sonic and Ramsay Healthcare have bought well and have continued to grow acquired businesses through successfully exporting their managerial approach and strategy. This somewhat differentiates the Australian healthcare sector relative to failed offshore forays made in other sectors (financials springs to mind).

Looking forward, we expect Australian healthcare will continue to present attractive investment opportunities supported by strong structural drivers (growing and aging population, the increased prevalence of chronic conditions and the availability of innovative new treatments that improve health outcomes) and the ability to continue to develop innovative new products that improve patient outcomes and increase the addressable market.

Author: Stuart Welch, Portfolio Manager