The COVID-19 pandemic has been a testing and turbulent part of our lives for what now seems like an eternity. But for some, this challenging period can be a gift, encouraging us to forge a new path, take a risk, and listen to that little voice within.

For Alphinity’s Global Portfolio Manager, Mary Manning, the pandemic brought about the realisation that her true passion was sustainable investing. Soon after, she announced her departure from her role at Ellerston Capital, where she had managed its Asia-focused strategies for nearly a decade.

“I’m Canadian and Wayne Gretzky is one of the country’s most famous hockey players. And one of his most famous quotes is, ‘You want to skate to where the puck is going, not to where the puck has been’,” Manning says.

“When I look at the investment landscape, I think sustainability is where the puck is going. And I think global is where the puck is going. So to have the ability to work for a global sustainable fund is really important to me.”

She has since nabbed a role with Alphinity Investment Management, where she works with a team of portfolio managers across its Global Fund and Global Sustainable Fund.

In this profile, we discuss seven valuable lessons that investors can draw on in the current market environment, including the role of technology in the transition to a sustainable future, why it’s important to be aware of the risks, and why you should draw on those around you.

Note: This interview took place on Friday, September 17th, 2021. You can watch the video or read an edited summary below.

1. Follow the puck

Whether you like it or not, sustainable investing is where the world is going, Manning says.

Following the “puck”, as Gretsky would say, she jumped at the opportunity of a fresh focus on global equities at Alphinity, with environmental, social and governance factors (ESG) in mind. It’s part and parcel of who she is, so why not apply this to investing?

“From a personal perspective, sustainable investing really aligns with my value system. I recently did a course with the Cambridge Institute of Sustainable Leadership, which if anyone has some time on their hands during lockdowns, I highly recommend,” she says.

“They actually take you through quantitatively why you care about sustainability. And for me, there were some very specific personal alignments, which was quite illuminating.”

However, before an investor gets kickstarted on their sustainable investing journey, it’s important to self-reflect and question the purpose of these options in their portfolio, she says.

“Is the main point just to get exposure to green things and green investments and make people feel better about themselves and their investments? Or is the point to have good investments, which are also sustainable?” She says.

No matter how sustainable, or how “green” a company, the investment case has to be there, Manning says.

“We are not just going to invest in companies simply because they’re sustainable and they look good on your top 10 and they tell a good story about sustainability. In every single investment that’s in the portfolio, the investment case has to be there,” she says.

There is a world of opportunity out there, Manning explains, one that isn’t just restricted to “green” companies like renewables or developed markets.

“One of the reasons why I’m excited to be involved with Alphinity is the process; the ESG process, and the structure of aligning a company’s revenues and their business operations with the Sustainable Development Goals (SDGs), is applicable across (different) markets and … different sectors,” Manning says.

“I think that’s important for a global fund because you can’t have double standards or triple standards based on where a company is operating.”

Renewables, for example, are a great story. However, a lot of these companies are “just not attractive investments”, Manning says.

“If you go back to the classic MBA Porter’s 5 Forces sort of analysis, there are either very low barriers to entry – this is part of the reason why the entire solar industry, particularly in China, is just not a good investment. Or there are extremely high barriers to entry and extremely high regulation. If you look at some of the wind companies in Europe, they’re in that basket,” she says.

For this reason, a lot of the traditional renewable plays “don’t stack up” from an earnings perspective, making it “a challenge to invest there”, she says.

“Where we found more interesting ideas in the green space is in industrials,” Manning says.

“Industrials play a very important role in respect to the energy transition, which gets overlooked by the more obvious stories in renewables. Schneider Electric (EPA: SU) is a French company, which we own, which is an absolute leader in terms of the energy transition. And it’s certainly a green stock, but it’s not maybe an obvious one.”

2. It’s a difficult time to be investing in China…

As many of you may know, it is not the easiest time to be investing in China – both thanks to the current Evergrande saga, which you can read about here, as well as the country’s widespread crackdown on a range of sectors, including tech, entertainment, education, property, ride-sharing and bitcoin.

“I would say that the reasons why it’s difficult are multifold. First of all, this regulatory crackdown is not just in one sector,” Manning explains.

“We’ve seen that before; a few years ago, there was a crackdown on online gaming and companies like Tencent (HKG: 0700) and NetEase (HKG: 9999) were not getting games approved. And you’ve certainly seen in the past crackdowns on the real estate sector or on gaming in Macau.

“But the thing about this regulatory reset is that it is ubiquitous. It is across every single sector. And it’s not even from a financial perspective; it’s across every single aspect of Chinese society.”

So from a stock-picking perspective, there is nowhere for investors to hide, she says.

“In other regulatory crackdowns, if it was in one sector, you could just reposition your portfolio elsewhere,” Manning says.

“That is not an option in this crackdown. And I think that’s a very big challenge for investing in China overall.”

There is also very little visibility on how long this “regulatory reset” could last, she explains, creating further uncertainty for investors.

For example, the crackdown on gaming – as mentioned above – lasted for 12 to 18 months. Meantime, the crackdown on political corruption or graft, introduced after President Xi started his first term, lasted for about three years, Manning explains. The cultural revolution lasted even longer, she adds.

“When people are looking at this regulatory reset in China, it’s hard to tell whether we’re 10 months in and this is only going to last for 12 months, or whether this is going to last for many years,” Manning says.

“The combination of those two things; the ubiquitous nature across all sectors, and the fact that the timing could be quite prolonged, makes it quite difficult to invest in China right now.”

However, when the dust settles, there will be some fantastic buying opportunities across large tech and consumer companies in China, Manning adds.

“But I think that right now, it’s still a little bit in ‘falling knife’ territory and a little bit too early to step in, particularly for a global fund that doesn’t have to have exposure to China,” she says.

3. But there are still opportunities in other emerging market economies

Manning believes that the structural growth story in emerging markets is a very attractive investment opportunity, noting that there are several companies within these markets that should have a place in every global portfolio.

She points to MercadoLibre (NASDAQ: MELI) as an example, which – for transparency – is held in Alphinity’s Global Sustainable Fund.

“It is the Alibaba of Latin America, but it’s not just e-commerce; they’ve moved into payments and they’re really democratising a lot of things in Latin America, whether that’s consumption or whether that’s financial inclusion,” Manning says.

There are also several mainstays in India, which is going to become “one of the top three economies in the world by 2030”, she says.

“There are some very high-quality companies in India, which I think are interesting. Certainly, HDFC and HDFC Bank (NYSE: HDB) on the finance side and the financial inclusion angle for those companies is quite interesting,” Manning says.

“Some of the IT services companies, which are best in class, Infosys (NSE: INFY) and TCS (NSE: TCS). And then Reliance (NSE: RELIANCE) – obviously the energy business is not particularly sustainable, but that company is going to get broken up into three different companies. And when it does, I think the telecom piece and the retail piece look very interesting.”

There are also several unicorns popping up in some of the smaller emerging markets, like Indonesia and Singapore, she says.

“Not right now, but maybe two to three years from now, once these unicorns have listed and they are profitable and they have a really good track record of being listed companies, they’re going to be must-own, or certainly must-look-at companies in emerging markets,” Manning adds.

4. Not all tech companies are created equal

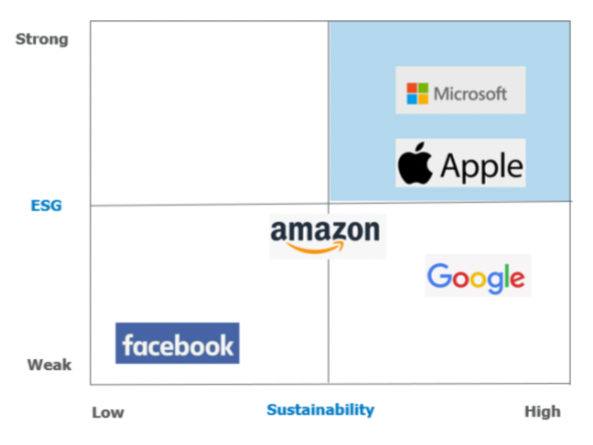

There is a big difference between the sustainability and ESG of the world’s biggest tech companies, Manning says. In fact, there is a large divergence.

“We’ve actually developed a matrix at Alphinity that looks at the big tech companies on those two metrics: sustainability, do they align with the Sustainable Development Goals, and then ESG, what are their practices? Are they best practices or are they severely lacking in practices?” She explains.

Sustainability / ESG Matrix for Big Tech

Source: Alphinity

As demonstrated in the matrix above, Microsoft (NASDAQ: MSFT) and Apple (NASDAQ: AAPL) are both highly aligned with the SDGs and also have strong ESG practices. Both of these businesses have a heavy focus on digital supply chains, particularly Microsoft, which means they do not have as large an environmental footprint, Manning explains.

Meantime, there are both positive and negative attributes of Amazon (NASDAQ: AMZN) and Google (NASDAQ: GOOGL) (for this reason they sit closer to the middle), while Facebook (NASDAQ: FB) demonstrates poor ESG and does not align to the SDGs, she says.

“On ESG, you need to remember that Google and certainly Facebook have dual shareholding structures. And so there’s a big differential between the economic ownership and the voting power,” Manning explains.

“Facebook is in the worst category here because Mark Zuckerberg is obviously still involved in the day to day and he also has significant voting control… it is in a class of its own in terms of having that ESG challenge.

“Whereas Amazon doesn’t. It’s a single shareholder structure and Jeff Bezos is actually no longer the CEO. While he does have an economic interest, it’s not disproportionate.”

She agreed that there has been significant negative press covering the treatment of Amazon’s workers, and notes that the gig economy and its sustainability is an important conversation that isn’t unique to Amazon.

“It’s Uber, it’s Lyft, it’s Meituan in China, it’s Swiggy in India. The gig economy and the impact on younger generations, Millennials or Gen Z, and how that’s changing how they work is actually a big piece of work that people still need to get their heads around,” Manning said.

“We did a lot of work on this with respect to Amazon, and it is better than a lot of peers. Amazon is a company that is, at the current time, not in the sustainable portfolio for that reason. But it’s certainly something that we are watching and as they make improvements, it may become eligible to be in the sustainable portfolio.”

5. But technology does have a role to play in the shift to a sustainable future

While there is a range of good, bad and ugly when it comes to sustainability and the tech giants, Manning believes technology can be a powerful enabler for sustainable development.

“Financials is a fantastic example because I mentioned HDFC and HDFC Bank before in India; their digitization strategies and the hundreds of millions of people that they can reach via FinTech is something that would just be impossible without technology,” she says.

“The company I mentioned before, which is in the sustainable portfolio, MercadoLibre – the democratisation of payments and consumption in Latin America and being able to access people in lower-income communities and certainly in lower-income countries, that’s only available because of technology.”

In addition, the power of technology across education and healthcare has become more evident during the COVID-19 crisis and has significant potential in developing countries to deliver services that communities may otherwise not have had access to, she says.

“The last sector that I’ll call out is agriculture. So we own Deere & Company (NYSE: DE), which is a leader in terms of precision agtech. If you think about what that can do over time in terms of helping farmers and aligning with SDG 2, which is ending hunger, then that’s very powerful,” Manning says.

“When you’re thinking about technology and sustainability, it’s not just, do I like Facebook or not? Or, do I like Microsoft or not? It’s, what is technology, as a driving force, doing to enable other countries and other companies to become more sustainable in their operations?”

6. Know the risks

With many of the world’s major economies’ cash rates now sitting near or at zero, Manning believes the biggest risk to markets is policy error.

“COVID-19 really put the whole world at zero interest rates and most of the developed countries, not just at the zero bound, but certainly in QE,” she says.

“This is very tricky for everybody. It’s tricky for us, it’s tricky for your readers and your viewers, it’s tricky for Jerome Powell. It’s tricky for policymakers around the world. And so I think that the biggest risk is that there’s a policy mistake.”

From a global perspective, and particularly in the US, that mistake could be twofold, Manning says:

- The first, is that central banks are worried about stalling global growth as well as further waves of COVID-19 and keep interest rates too low for too long.

- The second, is that they taper bond purchases and raise interest rates too fast, and that just chokes the economy off. There is the possibility then, that the major economies of the world get stuck at the zero bound forever.

She also believes that supply chain disruptions will continue to be a risk for markets, arguing that in the third quarter this could be the “biggest swing factor and potentially the biggest surprise in earnings”.

“There’s been the chip shortage in semiconductors, which has been going on for quite a while now,” Manning says.

“You had that whole pull forward of digitalization because everybody was working from home and schooling from home, and every single company in the world needed to go online very fast … And that had an incredible increase in the amount of demand for semiconductors.”

At the same time, many factories around the world have had to close in the face of the pandemic, causing further a supply/demand imbalance, she says.

“Even though a lot of countries have come out of COVID, that supply/demand imbalance has never gone back into balance … And that’s still ongoing,” Manning says.

“I had a call last night with a German company called Infineon (ETR: IFX). And they’re saying (it will be) 2023 before that semiconductor supply/demand imbalance is back in whack.”

New strains and outbreaks have also had ramifications on transportation and some of the world’s major ports, she says.

“Even if you shut a major port in China for two days, that could have a major impact,” she says.

Meantime, we are also seeing labour market issues across various global economies

“You can’t find enough people to work at ports. You can’t find enough warehouse space… So as a result, you’re getting significant backup in supply chains,” Manning says.

“The combination of those two things, semiconductors and logistics, means that a lot of companies just can’t get their goods. And that’s going to have an impact on both sales and on costs in the second half of 2021.”

7. And draw on experts around you

Manning has had some fantastic mentors throughout her career, having landed a role with George Soros on finishing business school at Soros Fund Management, and later working with the legendary Howard Marks at Oaktree Capital.

From Soros, she grasped that it is important to never stop learning.

“If you’ve seen George, he’s on TV, he’s in his eighties now, and he’s still talking about China and still talking about investments. That’s been 60 years of learning about investment opportunities,” Manning says.

Every opportunity when investing should be approached as a learning opportunity, Manning says.

“I would just encourage your readers and your listeners to keep learning. It’s why I mentioned the course I did before at the Cambridge Institute for Sustainable Leadership. Because I want to learn more about sustainability and there are lots of interesting things going on,” she says.

From Marks, she realised that writing things down is incredibly important.

“His memos are now famous and they’re read by millions of people around the world,” Manning says.

“The power of having that clarity of thought which comes from writing things down and thinking things through and having a record of how you were thinking and how that played out, I think, is very powerful.”

Putting her money where her mouth is, Manning is now emulating Marks at Alphinity, writing down her thesis and any changes for each investment.

“For investors at home, just writing stuff down is a good idea,” she says.

Manning also believes collaboration and healthy debate can massively benefit investors. She recommends readers draw on those around them, whether that be colleagues, friends, or even other investors here on the Livewire platform, to find new ideas. Speaking of her new role at Alphinity Mary says:

“One of the things that I really love about the firm is that it’s a co-PM model,” she says.

“To be able to deliberate with your peers, debate things and have people who are very smart that you can talk to and throw ideas around, that’s one of the things that I learned from the people at Alphinity in the early days of being there.

“Having a group of people whose intellect you respect that you can talk to about stocks and investments, I think is really important.”